Gold, post-bubble, is a reflection of just how bad things are, and it’s likely to get much worse

My long-held opinion is that gold does little aside from anchor a sound monetary view in a Keynesian debt world gone mad. For decades, as the Keynesian way (credit/debt leveraged for growth) has been THE way, it has come to be taken for granted by the masses.

Hence, the widely accepted notion of a centralized monetary authority that manipulates interest rates – thereby manipulating money – in service to micro-managing an economy that should be left to its own natural devices (a quaint and seemingly out of touch notion, I grant you).

The Fed and the Keynesian system it stewards are responsible for the great wealth disparities in society, as monetary policy (with routine assistance from governmental fiscal policy) has rigged asset prices higher, thus rigging the wealth of asset owners higher. While the resulting inflationary effects have pushed paycheck-to-paycheckers to the breaking point.

I made the point in NFTRH 859 (and many times prior) of a post-bubble environment in which gold would be revalued…

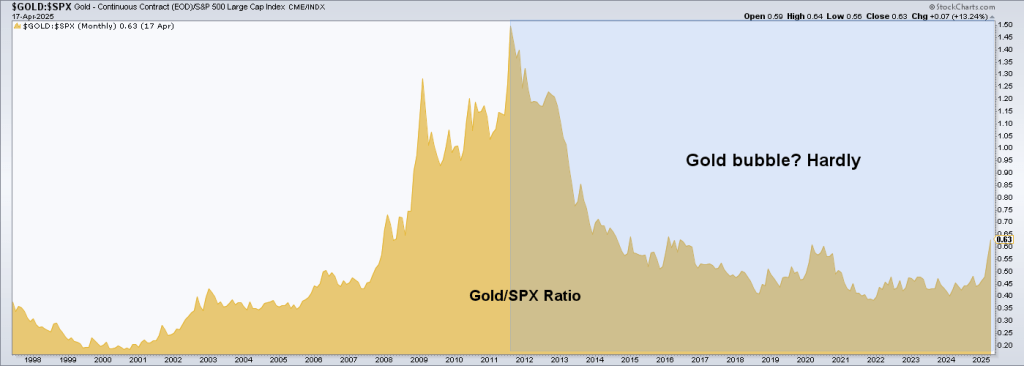

And then there is this chart, which I keep front and center to remind myself of the macro that was, robo-inflated by a 20 (+/-) year run of bubble making by monetary and fiscal policymakers, and the macro that is, post-bubble, with gold like a beach ball held under water, finally released.

Gold/SPX is on a spike, which with not much positive macro news (on trade, war, earnings, what have you) could be repelled if the stock market’s rally, bear market rally (BMR) or otherwise, has more upside off of the recent mega bearish sentiment extreme. But the main takeaway of this picture is that gold has a lot of catching up to do in its bull market relative to SPX. It is only now coming out of its base.

To my eye, the situation in Gold/SPX looks like the initial move in 2000-2003, fitting nicely with other aspects of our 2001-2004 analog theme.

Gold is Monetary Value

It is so simple, it usually gets lost in the noise of a gold bear market or a gold bull market.

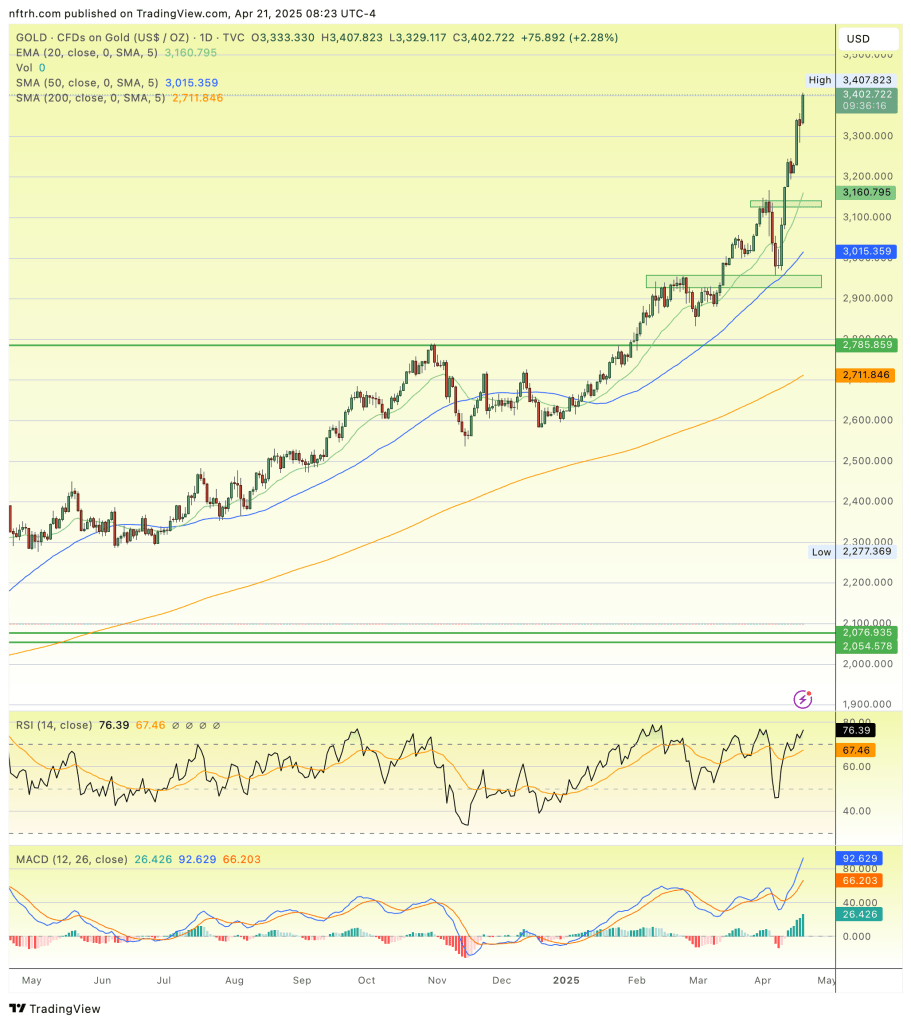

The point being that the value proposition of gold does not change. It was the same when the linked article was written in 2007 as it was during the worst of the monetary policy bubble circa 2012-2022, and today, as gold’s nominal price does this…

The price of gold is going to correct. It will happen tomorrow, next week, next month, or some other time. It is going to correct from a price with a 3-handle, or maybe even a 4-handle. And when it does correct, the move is going to be harsh. But that will only be felt by those FOMO’ing and MOMO’ing gold as a price vehicle, a plan,y or a speculation on global strife.

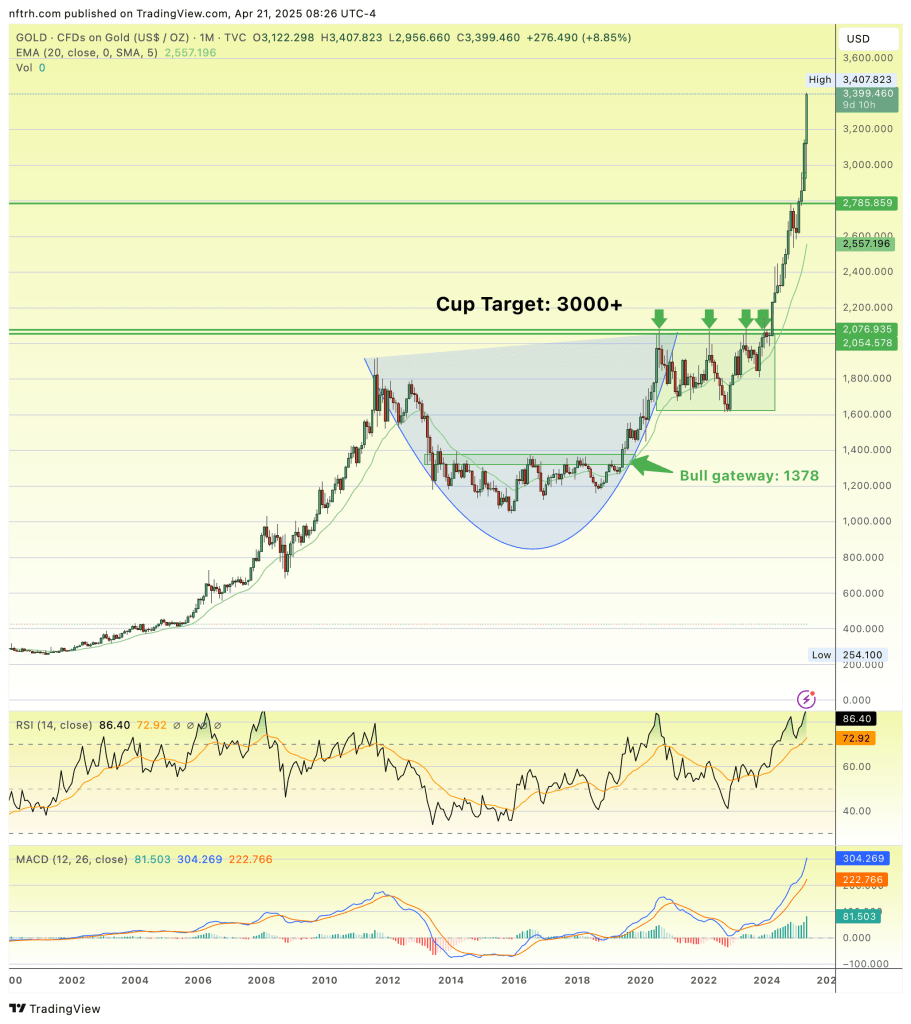

You can bet that animal spirits are in play now that gold has absolutely destroyed our long-held target of 3000+.

MOMOs always push things higher than you’d imagine. But keeping a view of gold as simply a reverse indication of confidence in the Keynesian system, as insurance against that failing system, will provide refuge when the going gets tough for the “price” assigned to gold’s long-term “value” at any given time.

The Gold/SPX chart above advises that there is a very long way to go in this new macro, inevitable gold price corrections included. “Price” is not value.

About the author