A SYSTEM OF ORDER

For the most part we are the beneficiaries of orderly financial markets. For more than two hundred years market makers and traders have bought and sold – for themselves and in behalf of others – without long-term disruptions to the orderly function of markets.

Clearing brokers accommodated the increase in participants and trading volume. Technological advances have added layers of efficiency and convenience that can seem unbelievable.

With an online brokerage account and a smart phone, nearly anyone can place a trade instantly. Execution of a simple buy or sell order at market is executed almost simultaneously. The speed is mind-boggling – to some of us anyway.

WHAT CAN GO WRONG?

Pretty much anything. That does sound harsh, so let’s refine the answer a bit and introduce some qualifications.

One of the most critical factors to consider is to ask how likely it is that a particular event or series of events can occur. In addition, we need to think about how the event(s) would affect us specifically. Finally, what is the extent of our vulnerability, both individually and collectively.

For example, how negatively would you be affected if you couldn’t use your smart phone to place a trade? If that doesn’t seem to be too big an obstacle, take it a step further and imagine that use of all smart phones for securities transactions was disabled. Lastly, what would you do if all the technology that we are so dependent on wasn’t available?

If your thoughts about these things worry you, then you are farther along towards dealing with them in adequate fashion should they occur. If you are confident that something like that cannot happen, or will not happen, then you are likely more vulnerable than you know.

What if the financial markets were to drop by two-thirds or more from current levels and stay there?

From their all-time peak (at that time) in August 1929, stocks lost almost half of their value in slightly more than two months. After a partial recovery lasting five months (up to April 1930) that left stocks still down by twenty-five percent from those pre-crash highs, stocks descended into an abyss that seemed to have no bottom.

There was a bottom of course, but it took two more years to find it. By that time, July 1932, stocks had declined ninety percent from their peak prices in August 1929. The entire affair from peak to trough lasted less than three years. See Chart No. 1 below…

Chart No. 1 Dow Jones Average – 1929 Crash and Bear Market

With all of the current focus on the potential Fed pivot, and the prospects for stocks now, it might be worthwhile to see how the current market action compares to 1929-32.

STOCK MARKET TODAY

Measuring from the peaks for most stocks in December 2021, prices declined by twenty-five percent over the next nine months. The NASDAQ Composite Index lost more than one-third of its value between December 2021 and December 2022.

With a partial recovery over the past couple of months, stocks are still down twenty percent or more from their December 2021 highs. The NASDAQ Composite is currently down twenty-six percent.

Price action similar to what happened in 1929-32 could take stocks down by another eighty-five percent from current levels. For the NASDAQ, that could mean an index quote of 1500; or a DJIA of 4000.

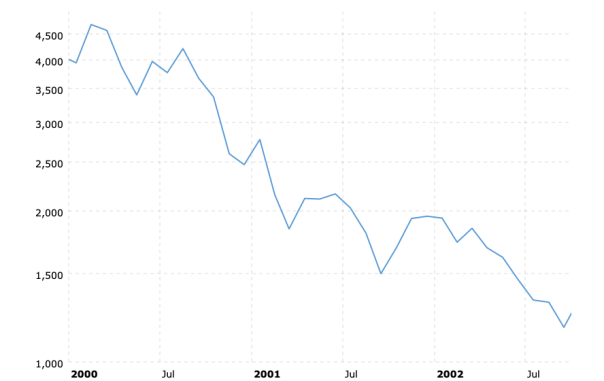

The markets showed us something similar two decades ago. See Chart No. 2 below…

Chart No. 2 NASDAQ Composite – 2000-2002

The time frame for the “dot.com” meltdown and NASDAQ stock crash was similar to that which occurred in 1929-32. In less than three years (32 months) stocks fell nearly eighty percent.

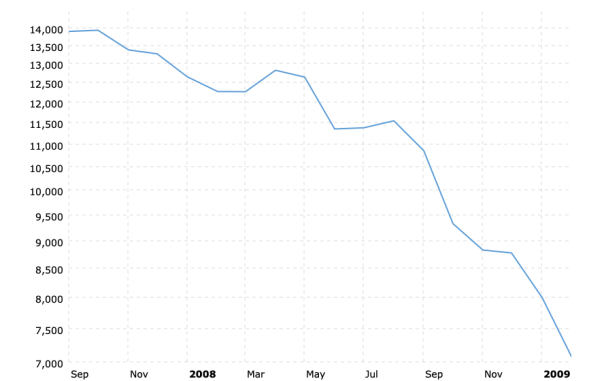

Not to be outdone, the Dow Jones Industrial Average led the way down a few years later. See Chart No. 3 below…

Chart No. 3 Dow Jones – DJIA October 2007 – February 2009

Over a period of sixteen months, the Dow Jones Average from peak to trough declined by fifty-four percent.

WHAT HAPPENS NEXT TIME?

After stocks crashed and the ongoing Great Depression deepened, stock trading activity came to a standstill. Watching the ticker tape became a distant memory. Brokers and advisors who were still in the business recommended bonds to their clients – if they had any money left. (Not today!) Stocks were considered literally to be the kiss of death.

It took more than twenty-five years for stocks to get back to their pre-crash levels. Allowing for the effects of inflation, it took thirty years. Not until November 1959 did stocks reach and exceed their pre-crash level of August 1929.

Something like that can’t possibly happen today, though; right?

THE WORST THAT COULD HAPPEN

We don’t know the worst that could happen, but however bad it gets, it will be worse than the 1930s and worse than anything we can imagine.

Part of the reasoning for expecting “the worst we can imagine” stems from the broad exposure and vulnerability to catastrophic market conditions that exist today.

People expect that Fed policy and actions will make everything better if things get out of hand. Maybe it is out of their control. Or, maybe their game plan and expectations are different from ours.

Whatever you think about the Federal Reserve and the United States government, bad things tend to be worse than expected and last longer than necessary when the government (and central banks) are involved.

WHAT IF THERE IS NO MARKET?

What happens if things are so bad financially and economically that there is no “orderly market”?

We think we know how much something/anything is worth; but can you imagine how difficult it might be to agree on a price and execute an exchange for any goods or services in the midst of collapse in the financial markets, broad-scale economic depression and wide-spread social unrest?

For that matter, how will you take profits on your “successful” trades?

CONCLUSION

We talked about stocks earlier but let’s not forget that all assets are inflated to a degree that makes them vulnerable to huge declines. We are seeing this happen now and it includes bonds, real estate, and commodities, as well as stocks.

Inflation and intervention in the markets by government and the Federal Reserve have led us to a continual state of volatility and vulnerability which is characterized by dependence on credit and illiquidity in all markets.

Deterioration on all fronts is upon us. That does not bode well for a system of order. Chaotic breakdown is the more likely outcome.

(also see: A Depression For The 21st Century and Default-Deflation-Depression)

Kelsey Williams is the author of two books: INFLATION, WHAT IT IS, WHAT IT ISN’T, AND WHO’S RESPONSIBLE FOR IT and ALL HAIL THE FED!

About the author

Analyst, Author, and Owner of Kelsey's Gold Facts

Kelsey Williams has more than forty years experience in the financial services industry, including fourteen years as a full-service financial planner. His website, Kelsey's Gold Facts, contains self-authored articles written for the purpose of educating and informing others about gold within a historical context. In addition to gold, he writes about inflation and the Federal Reserve.

Kelsey is the author of two books: INFLATION, WHAT IT IS, WHAT IT ISN'T, AND WHO'S RESPONSIBLE FOR IT and ALL HAIL THE FED!

Kelsey Williams is available for private consultations, public speaking, and interviews at kwilliams@kelseywilliamsgold.com