At the end of last week's post, we promised to speculate this week on where I think this discussion might be headed in the weeks and months ahead. Let's dig in.

First of all, if you missed last week's article, here's a link:

• https://www.sprottmoney.com/blog/possible-gold-price-revaluation

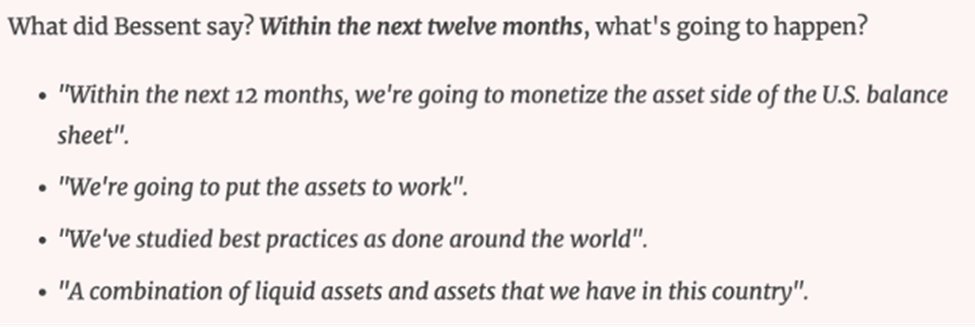

Key Statements from the U.S. Treasury

For the past several weeks, we've been focusing on statements made by the U.S. Treasury Secretary Bessent while standing beside Trump in the Oval Office on February 3. The occasion was the signing of an Executive Order regarding the creation of a Sovereign Wealth Fund. The key statements made by Bessent that day were as follows:

Bessent has since added that "revaluing gold wasn't on my mind" when he made those statements, so I guess we'll take him at his word. However, as we wrote last week, other than gold, what "assets" does the U.S. have on its balance sheet to monetize? As such, let's speculate this week on what may be coming "within the next twelve months".

Trump, Judy Shelton, and the Case for Gold-Backed Bonds

Does the name Judy Shelton ring a bell? Trump nominated Shelton to the Board of Governors of the Federal Reserve back in 2018, though her candidacy was eventually shot down by the U.S. Senate. Apparently, her beliefs in sound money were too "controversial" at the time.

• https://www.politico.com/news/2020/11/17/senate-rejects-move-to-advance-trump-fed-nominee-437067

Anyway, I remind you of this so you understand that Trump and Shelton are well acquainted, and he's obviously quite familiar with her policy suggestions.

Fast forward to 2025. Trump is POTUS again and here's Judy Shelton writing about her idea of issuing very-long-term U.S. treasury bonds:

• https://www.nysun.com/article/a-250th-anniversary-gift-for-uncle-sam?member_gift=CUZ5qwd3crq4pmz-xrd

The Problem with Traditional Debt Expansion

Now stop for a second and consider what interest rate you would demand for a 50-year investment in a U.S. treasury bond. Given the current fiscal situation in the U.S. and given the guaranteed loss of purchasing power that your principal would see while it's tied up for 50 years, would you demand a 10% coupon? Maybe that's too low? Perhaps you'd demand an interest rate of 15% or more before you would consider such an investment?

But what if your principal was backed by, convertible, or simply indexed to the price of gold? This would alleviate your concerns about loss of purchasing power over time and, as such, you might be willing to accept a 3-5% interest rate instead.

You might counter and say that the Treasury has already tried this with Treasury Inflation Protected Securities, or TIPS. However, TIPS are only indexed to CPI inflation and therefore struggle to keep up with actual purchasing power. A bond backed or indexed with gold would be an entirely different animal.

Could a Sovereign Wealth Fund Be the Answer?

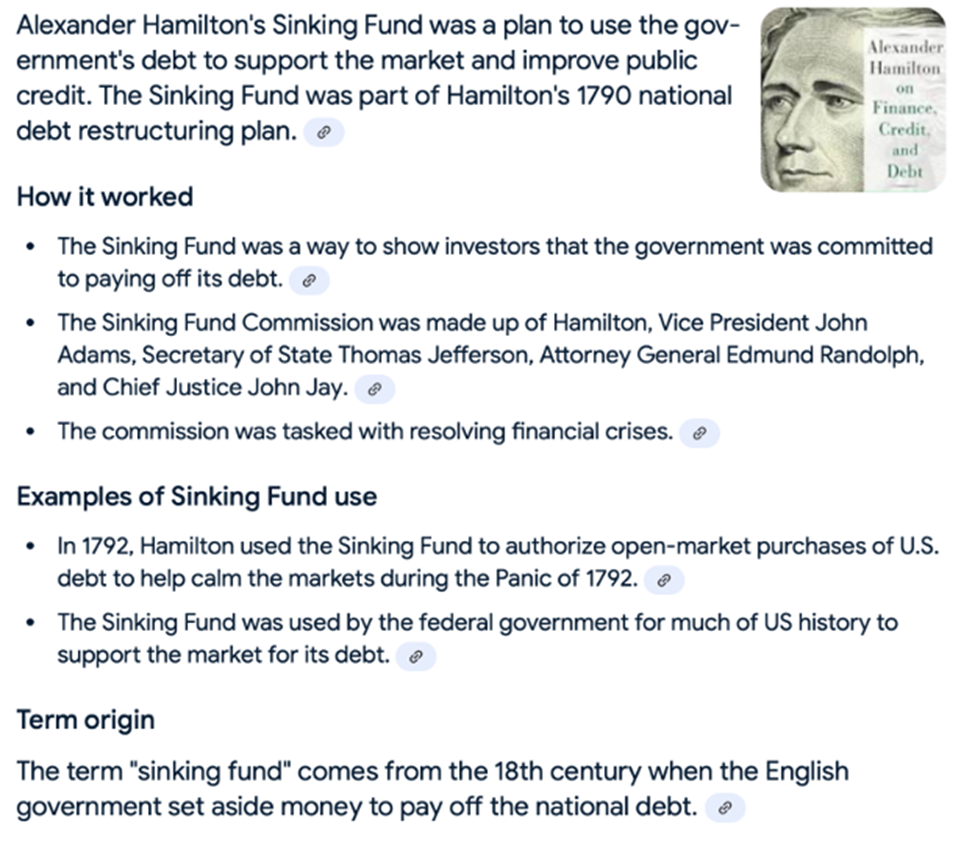

So now let's get back to Trump's executive order regarding the creation of a sovereign wealth fund. This sounds like a fine idea, and a sovereign wealth fund might eventually be utilized as a 21st century Hamilton Sinking Fund that could be accessed to purchase and eventually retire some of America's massive debt.

But how does Trump "fund the fund"? By issuing an additional $2T in traditional treasuries, Trump simply adds $2T to the current debt/deficit, which is already on pace for $2T in new debt this year. Running this year's deficit to $4T would seem like a political non-starter.

Hmmm. What a conundrum. But what if the new sovereign wealth fund was funded with $2T of 50-year bonds, specially issued and backed/indexed to gold in order to keep the annual interest cost low? That might work.

The Role of Gold in Future Financial Strategies

But first, you'd have to get some/most of your gold back onshore:

https://www.cnbc.com/2025/02/28/us-gold-demand-is-sucking-bullion-out-of-other-countries.html

You might then want to inspect and audit what you have in order to assure the investing public that your new bonds really are fully backed and/or indexed to gold:

The only remaining step would be to revalue or mark-to-market the gold you hold "on the asset side of the balance sheet":

https://finance.yahoo.com/news/gold-revaluation-risks-messy-outcome-181642849.html

What Happens If Gold Is Revalued?

Revaluing gold to $2800/ounce "creates" about $750B for your fund. Revaluing it to $10,000/ounce gets you north of $2T, and now we're getting somewhere. This would not imply that gold would immediately trade at $10,000/ounce. Instead, it's simply an accounting entry to give Treasury the "room" to create $2T in new debt.

Regarding the market price of gold, seeing the U.S. follow this path might lead other countries to "monetize" some of their own gold in such a manner. This increased demand for gold as well as the perceived "remonetization of gold" would almost certainly lead to higher bullion prices. Maybe not a $10,000 price, but likely not $2,800 either.

So, anyway, those are my thoughts on where this is headed. Could I be dead wrong? Of course! Like every other analyst in the precious metals community, I'm simply trying to connect all the dots of the news flow and price action since December. I hope that this week's column has given you some food for thought.

About the author

Our Ask The Expert interviewer Craig Hemke began his career in financial services in 1990 but retired in 2008 to focus on family and entrepreneurial opportunities. Since 2010, he has been the editor and publisher of the TF Metals Report found at TFMetalsReport.com, an online community for precious metal investors.