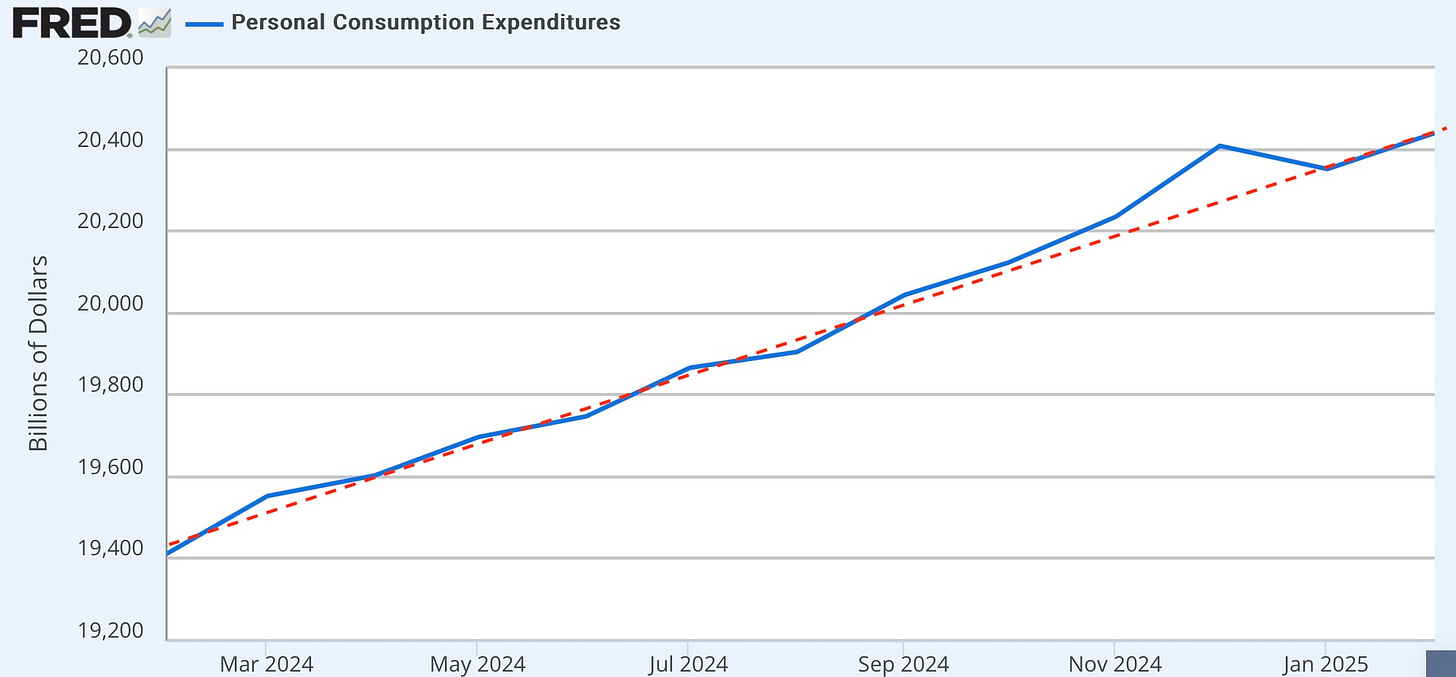

Core PCE inflation (the Fed’s favorite) rose again to hit 2.8%. You may recall that recently I wrote about how a minor downtick of inflation didn’t mean anything because there are no straight lines anywhere in economics, and the downtick was not large enough to break the trend. Now, we see that affirmed by PCE inflation rising back up exactly into its long-term trend, which was never broken by the dip:

The Federal Reserve’s key inflation measure rose more than expected in February while consumer spending also posted a smaller-than-projected increase, the Commerce Department reported Friday.

The core personal consumption expenditures price index showed a 0.4% increase for the month, the biggest monthly gain since January 2024, putting the 12-month inflation rate at 2.8%. Economists surveyed by Dow Jones had been looking for respective numbers of 0.3% and and 2.7%.(CNBC)

No big news here, but confirmation that the tiny dips in inflation meant nothing.

What we don’t see yet, and I wouldn’t expect us to, is much indication that tariffs are causing inflation. In fact, nearly all of the upward pressure came from services continuing to rise, which do not get hit with tariffs.

It’s too early for added import taxes to raise the price of goods on the shelf. Those goods are not likely even on the shelves yet, and most of Trump’s threatened tariffs are still in their Lucy-pull-the-football stage of withdrawal. There could be some anticipatory raising of prices starting to bleed through, but most businesses will be reluctant to raise prices until they have to because one more significant factor in the news recently is that consumer spending is falling, as is consumer confidence. The two go hand-in-hand.

Consumers turning more sour on the economy

The plunge in consumer confidence and consumer spending means there will be a lot of “negative price elasticity” (flexibility/reactivity) between changes in price and changes in consumer purchases. This is the bad kind of flexibility for businesses wanting to price in added costs, such as tariffs: flex the price upward, and consumer spending bends downward. High negative elasticity is a strongly inverse relationship.

Inflation expectations are enduring, and that makes them typically a self-fulfilling belief because anyone doing pricing is expecting more cost increases, themselves, so looking for any chance they can to get away with price increases. Rising expectations indicate that inflation will continue to be sticky and likely rise, but the negative price elasticity is going to make that a tough tug-o-war with consumers.

The final March reading of the University of Michigan’s consumer sentiment survey found the mood worsening among Americans of all political persuasions.

The mood of consumers is turning ever more pessimistic as expectations about the future course of the economy slumped nearly 18% in March and are now nearly a third below where they were in November.

Meanwhile, expectations of where the annual rate of inflation will be a year from now surged to 5% from 4.3% in February. (US News)

That puts consumer expectations all the way back to where they were when the actual rate of inflation was still hot at 6.5%.

“This month’s decline reflects a clear consensus across all demographic and political affiliations,” said Joanne Hsu, survey director. “Republicans joined independents and Democrats in expressing worsening expectations since February for their personal finances, business conditions, unemployment, and inflation.”

Obviously consumers of all political persuasions are a lot smarter about inflation than the president and his team are because Team Trump keeps telling us unanimously that tariffs are not inflationary. In an environment where we continue to see that inflation is continuing to rise, there is almost no chance that upward pressure on prices from tariffs won’t move actual prices upward. So, you ARE going to pay for these tariffs, and you will likely keep paying for them for longer than the tariffs continue because prices tend to be NOT as elastic moving back down as moving up because companies only lower prices to the extent that competition forces them to, and they rarely back come down to what they once were.

Don’t worry. You’ll feel liberated from this threat on April 2nd when Trump’s tariffs supposedly will finally go into effect. (The tariffs with China already are in effect.) For right now, Canada and Europe are exacting more tariff damage on US exporters because they did not pull their retaliatory tariffs when Trump did a head fake and pulled his within 24 hours of implementing them. Trump is calling April 2nd “Liberation Day,” so get ready to feel liberated.

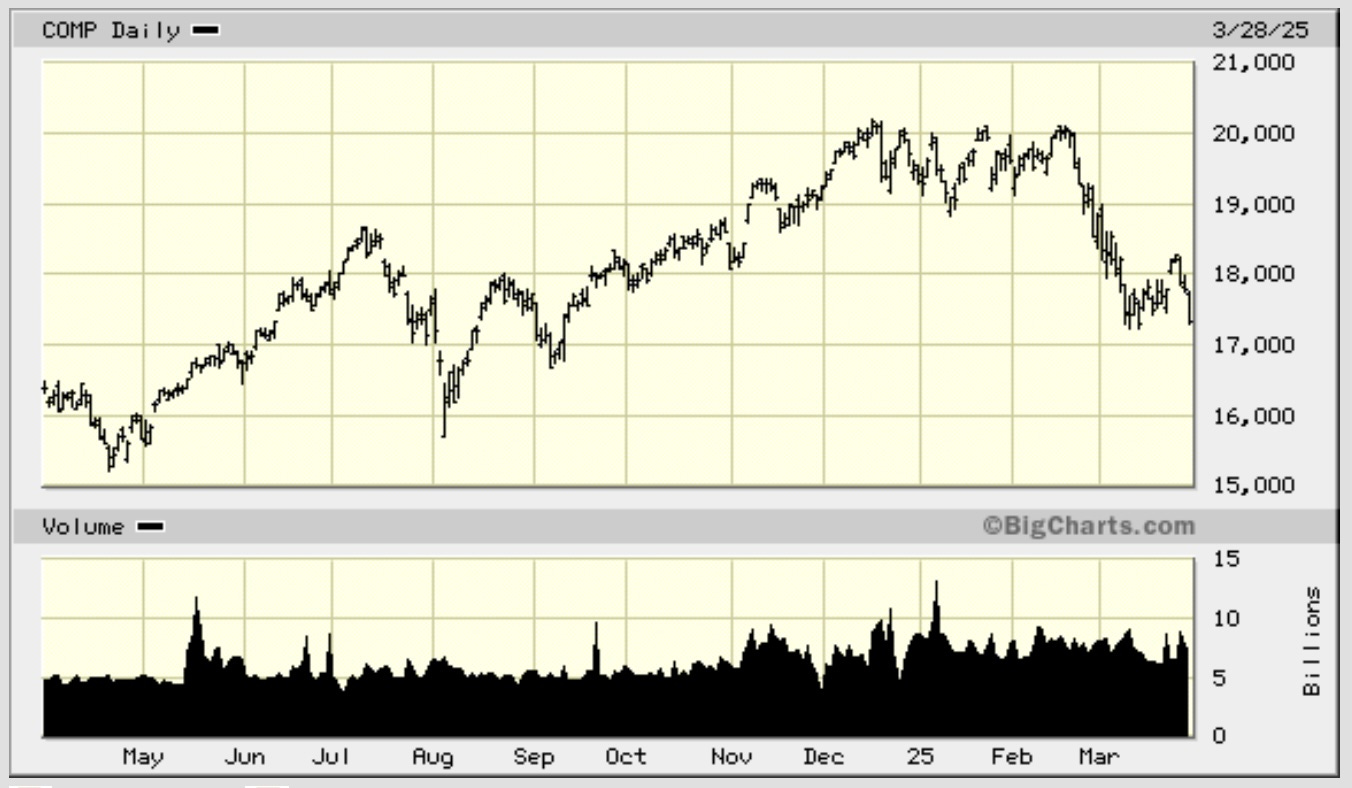

Already the stock market has sold off nearly 10%, and the Dow Jones Industrial Average was down more than 500 points Friday after a key inflation reading followed by the Federal Reserve came in above expectations.

Make that more than 700 points now that Friday is over (with the Nasdaq falling another 2.7% on Friday. The Nasdaq has seen a pretty sharp falloff since December, erasing a lot more than all of its post-Trump-victory gains, down 14% from its all-time high:

“Broadly though, it’s not just the fact that the rules of the game have changed that has dimmed the collective consumer mood, but the fact that there’s little clarity about what the rules will be when the dust settles or what the effect will be,” said Jim Baird, chief investment officer at Plante Moran Financial Advisors.

“When you don’t know what’s coming, it’s harder to plan,” Baird added. “In the face of growing uncertainty, consumers are left with tough decisions. In some cases that may mean accelerating purchases out of fear of even higher prices ahead; in others, it may translate to pulling back on spending altogether. In either case, the murky outlook weighs on confidence.

In other words, it’s the cost of chaos.

The rest of this article will lay out the most probable map forward into recession. It’s the same route I already laid out for paying subscribers, but it will show how precisely we are following that path already and why we will continue to do so. It is, at best, a path that leads to great stock-market volatility or, at worst, a fiery inflationary future, should the Fed and feds try to save the market with their typical past approach of printing their way out of market misery via more monetary misery.

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!