This day morphed into a do-everything-the-opposite-at-the-same-time kind of day. The morning started with loud screams of deleveraging everywhere, but the forces that groaned pitifully downward in the darkness at twilight suddenly flipped to heaving mountainously upward around noon. Hedge funds have been bailing out everywhere this week, but US Treasuries went from falling yields to yields taking off like a rocket this morning at an outrageous velocity that hasn’t been seen since 2008. Nations are fleeing US debt; yet, the recent 10YR Treasury auction blew the roof off most auctions. The stormy morning couldn’t have turned into a sunnier blue-sky day for such a huge close-out sale on the United States economy. What to make of it all?

Everything has been deeply troubled this week, and the trade war kicked into full gear overnight with China and the US both turning the heat way up; yet, stocks absolutely exploded like a lava fountain in a relief rally the likes of which have rarely been seen. The Dow blew upward a massive 2,900 points (+ almost 8%) and the NASDAQ was up an even more earth-lifting 12%.

So, what do I make of the earth-shattering contradictions that filled the news to both extremes? Let’s start with everything that has plunged and then end with the good and what to make of it.

The national debt bomb may be blowing up

The signs of national flight from US bonds absolutely dominated the early news, and that indicates nations are fleeing US dollars, as well, which fulfills another one of my economic predictions for 2025 if that is as it appears to be.

To get to the bottom of some of this enormously chaotic action, let’s start by going back to the major prediction that started the year. I wrote the following in a Deeper Dive, which I’ll share with everyone now that the prediction of something explosive appears in the process of being fulfilled:

“Trump Tariffs Could Be Nuclear Time Bomb for National Debt”

An unexpected chain reaction in the massive US debt is right on the horizon….

No one seems to see this coming; so, in this article, I’m going to show how the extremely high tariffs being promised by newly elected president, Donald Trump, could create a chain reaction that will become a nuclear US debt bomb….

As nations like China trade less with the US due to the inevitable impact from Trump’s promised tariffs … those nations will also have less need for the global trade currency; i.e., the dollar….

The way national banks exchange dollars is via assets valued in dollars where ownership can readily be moved cross accounts, such as bonds that are issued in dollars….

Less trade among nations equals less need for US Treasuries in central banks and other international banks because the use for Treasuries as currency exchange falls off a cliff.

As demand for Treasuries diminishes, the value (prices) of Treasuries will also diminish. As that happens, central banks and other international banks not only need fewer of them for interbank foreign exchange because their customers are doing less international trade, requiring fewer Treasuries to reconcile transactions via bank reserves, etc., but now the value of the Treasuries that banks hold in reserve will drop.

That, in turn, will make banks want even fewer of them—not just foreign banks, but also domestic banks because US Treasuries are a global market, being the predominant form of “the dollar” among banks; and declining values aren’t attractive to anyone using Treasuries in their reserves as a store of sovereign wealth or as bank reserves.

So, you have two factors here: one is how many Treasuries are needed for exchange on foreign trade and the other is how many are wanted for storage of sovereign wealth if they are declining in value….

A huge drop in foreign trade likely translates to higher interest on the US debt as old bonds are paid off at maturity and new bonds are issued to make the payoff possible….

Importantly, because the dollar is the most globally accepted trade currency, central banks (and other major international banks) move these “bags of dollars,” as we’re calling bonds, in exchange transactions between nations because those central banks serve their own nation’s businesses, which do endless trades with the massive consumer economy that exists in the US.

Tariffs turn that economy in the US into an internal circle that does far less foreign trade. Because the Trump Tariffs will hugely decrease international trade, as they are intended to do, they will also likely drive up interest on the US debt and likely be inflationary as well.

Currently, we see what I predicted in early January cracking through the surface of our economy. Treasuries had taken a brief plunge in yields as the tariffs began, which seemed strangely positive, but overnight that trade swung to the other extreme, and yields soared (by the usual glacial measure at which they change). As I mentioned, it was the biggest spike in yields (drop in bond prices) since the 2008 financial crisis when stock investors bolted to safety.

Major bond gurus also started to warn this week (in the news below) that deep trouble was about to break out in the bond world. At the same time, the value of the dollar in foreign exchange started falling quickly, indicating some of the fierce US bond selling that has pressed yields higher in the last twenty-four hours in order to attract new buyers was from foreign entities dispatching their dollars while Europe and Asia were trading ahead of the US.

And then we got this upheaval in a fantastic Treasury auction this afternoon. The earth is moving beneath markets in a way that is truly dizzying as investors try to figure out what to do and where to go.

Bonds were but a brief safe haven from crashing stocks

One reason yields had been falling was that money fleeing the US stock market faster than other national stock exchanges started by fleeing to US Treasuries as a safe haven. The plunge in stocks has beaten some historic measures. Can anyone see the waterfall:

The Dow and S&P both looked just as bad at the start of the day, but this afternoon’s relief rally recovered most of the waterfall, though it still leaves the market in a correction for the year. I’ll come to what to make of that below, but first: Some of that money fled into US Treasuries for a bit, but suddenly US Treasuries stopped functioning as a safe haven. There are several factors in force that make this a very dangerous situation for the US, but I won't start with a summary by bond guru Jeffrey Gundlach:

The Dow and S&P both looked just as bad at the start of the day, but this afternoon’s relief rally recovered most of the waterfall, though it still leaves the market in a correction for the year. I’ll come to what to make of that below, but first: Some of that money fled into US Treasuries for a bit, but suddenly US Treasuries stopped functioning as a safe haven. There are several factors in force that make this a very dangerous situation for the US, but I won't start with a summary by bond guru Jeffrey Gundlach:

“It’s going to be messy”

As Gundlach says, the market has now become truly disconcerting. It’s making frantic, messy moves in more than one direction. Here is the video followed by a summary of his comments:

I think somebody’s going to go bankrupt. Everything is flat or down except for gold…. This type of thing usually ends with forced liquidations, and I think they started last week, and we certainly see that this morning. There is going to be more deleveraging, and the Fed is really not in a position … to resume rate cuts because … people are looking for inflation … very opposite of what the Fed is hoping for…. The Fed can’t loosen up because of inflation concerns, and tariff concerns obviously compound that. Under three weeks ago … I told you I thought there was a 60% chance of recession. I thought that was way out of line with the consensus, which I think was more like around 30/35%... I think the consensus is [now] up to 50%... I can only raise my 60%.... I’ve been saying the market was ridiculously overvalued…. There is just a lot of room for this to normalize … which is a long way down based on the CAPE ratio…. It’s going to be messy. This looks like a deleveraging scenario, which can take on a life of its own. —Gundlach from the video above

Gundlach points out that, with over $ 20 trillion of foreign investment in US debt, foreigners divesting due to tariff wars means they don’t need so many treasuries to trade (and due to wanting to hurt us to get us to knock the tariffs off). That is just as I told my paying subscribers at the start of the year we would see from the Trump Tariff Wars. This becomes a risk to all debt that is based on Treasury rates but especially to the US debt, which has already been downgraded, and it turns the Republican congress’s latest budget into a failure to meet up to the dire situation.

Gundlach sees the sudden turn-around in the foreign bond trade as well as hedge-fund deleveraging as a big reason Treasury yields have gone back up, after coming down in an initial decline when money started pouring out of stocks. Now foreign money is selling bonds in net, which pushes yields back up in order to find enough domestic buyers. Of course, when yields bolt upward that attracts a sudden new round of investors back in. I’ve referred to it in the past as the bond pump where the handle goes up and down like a seesaw, pumping money from the stock tank into the bond tank.

Gundlach also says, as I have been saying repeatedly, that he doesn’t understand the “strange formula” the Trump administration uses to calculate its tariffs, which he sees as arbitrary, but he thinks Trump is going to keep creating this chaos because this is Trump getting even for all the chaos and lawfare that was done against him right from the start of Trump 1.0. In Gundlach’s view that means Trump doesn't care about the wreckage because he’s getting even; he’s going to keep pressing this to keep everyone else off-balance.

I, of course, have no idea if Gundlach is right about Trump’s motivations, but I do know there is no sense at all in the basis Trump has presented for his tariffs, but I won’t repeat my arguments about those chaotic calcs. If anyone doesn’t believe those arguments by now, they are not likely going to.

Bonds are the pits

Instead, let’s look at what is happening in actual bond action in the bond pits.

Conservative writer (old-fashioned conservative) Ambrose Evans-Pritchard warns in one of the articles listed in the headlines below that Trump is crashing the bond market. He expects Trump will find a way to fire J. Powell if Powell doesn’t bail out the US debt as it crashes due to the Trump Tariff Wars. He lays out paths Trump has taken to fire other people that are supposedly purposefully put out of political reach by Congress and by tradition to show how Trump can and will do the same with Powell if he doesn’t cooperate.

Does anybody in their right mind think that Trump will spare the Fed’s Jerome Powell as the two men gear up for an almighty clash over US monetary policy?

As foreign money now flees US Treasuries, the only way the US will be able to keep interest on its debt from rising over its eyeballs is if the Fed rushes back to massive QE and starts hosing up all the debt that foreigners are trying to get rid of.

According to Evans-Pritchard,

Powell told Congress that the tariff shock is much bigger than expected and may set off “persistent” inflation rather than just a one-off jump in the price level. He came close to damning Trumponomics as a recipe for low-growth stagflation. That is a red flag to a bull.

The current debate over whether or not Trump has the legal power to fire Powell entirely misunderstands the character of the Maga revolution. America’s rule of law is for guidance only these days….

[but]

Powell will not go without a fight. “I will never, ever, ever leave this job voluntarily until my term ends under any circumstances,” he said during Trump 1.0.

Means by which Trump could oust Powell have already been put forward by the loosely flapping lips of the nation’s own Treasurer—usually, a person who works in close concert with the Fed (not that I mind seeing that cozy relationship break, but just that it looks to be breaking) now that Trump encourages all of his staff to be as adversarial as possible:

Scott Bessent, the Treasury secretary, said the administration could sideline Powell by appointing a “shadow” Fed chairman, who could steer the markets by issuing forward guidance. But this does not overcome resistance from the Fed board and the hawkish regional presidents.

A secretive team of Trump loyalists drew up a 10-page report before the election proposing more radical measures. These include forcing the Fed to “align policy with administration goals” or even to make the president an “acting” member of the Fed board.

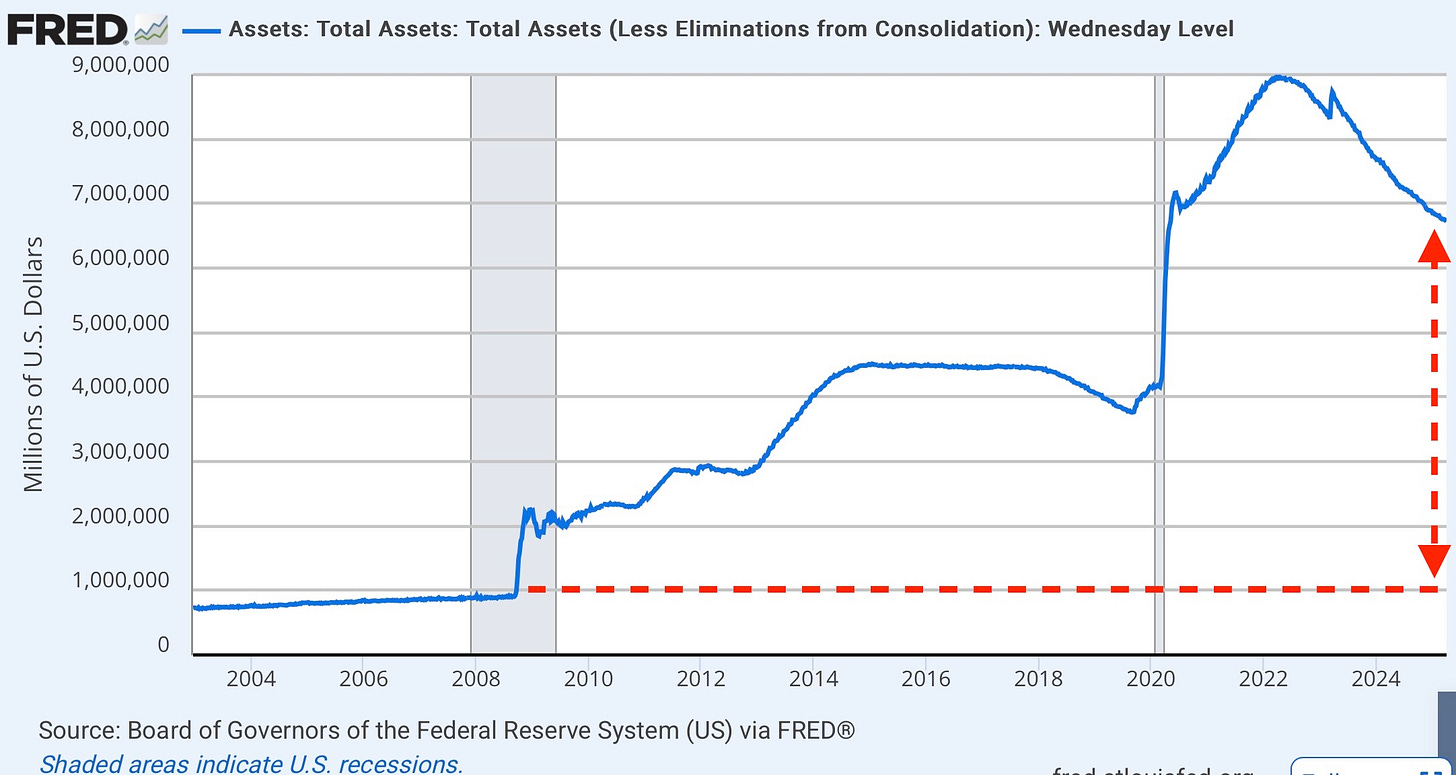

Trump will likely find a way to oust J-Pow when the US debt goes sour if Powell doesn’t jump in with Treasury buying, but I think Powell will do that on his own because the Fed has a longstanding, iron-clad policy of supporting the US debt by any means of monetizing it while claiming it is not doing so. (Notice that the Fed has long claimed it was not monetizing the debt with its massive QE Treasury purchases on the basis that they were just “temporary monetary policy,” as I’ve written about in the past.)

One of the things I warned about over and over years ago was that this lie would be proven, even if the Fed believed it when we got to see how unable they were to ever reverse QE. That promised reversal was the basis Ben Bernanke gave for claiming QE was not monetizing the debt. It was a temporary measure just to affect money supply and interest rates.

OK. So years later, look at where we are on reversing QE and making it temporary:

You can see the Fed tried to reduce its quantitative easing via quantitative tightening once before back in 2018 and 2019. That turned into a catastrophic failure that gave us a huge crisis in the normally quietest area of interbank finance—repo loans. The Fed backed out of its QT prior to Covid, and then Covid gave them the excuse to rush headlong out of it by doing the greatest volume of QE ever seen on earth. Now, we’ve gotten down halfway to the level where the repo crash happened, and the Fed has already started to taper its QT way back.

No, we’re never getting out of QE because it DID monetize the debt for good, and we cannot begin to undo that, especially now that the tariff wars are driving away our foreign investors that made that debt so cheap and affordable for decades. They don’t want us anymore. We are toxic to them, and our debt does not look safe when there are no trade reasons left to keep hoarding Treasuries as a vehicle for dollar exchange, which is why the dollar has begun to collapse, as also reported in recent headlines. This is why Russia is celebrating, as I reported: Trump is accomplishing what they were never able to.

Hence, Evans-Pritchard’s warning about the big bond bust that is in the process of happening. Since the Fed has always supported the US debt as a buyer of first resort when necessary in any amount necessary, I don’t see them as being willing to let the debt crash completely. However, QE is inflationary because it tends to expand the money supply and lower interest rates on long bonds. The latter would, in fact, be the intention.

However, the Fed can try not to lower that interest enough to be inflationary since merely keeping the debt from rising in cost is the goal, not stimulating the economy in a time of inflation. However, not adding to inflation just from the increase in the basis of money supply may be problematic in a highly pressurized inflationary environment of tariff-caused shortages. So long as the money stays out of consumer hands, that may be doable. This dynamic will be something we are likely going to need to keep an eye on here at The Daily Doom some months down the road, such as this summer when QE is likely to begin due to the rush out of bonds by foreign investors. If the Fed doesn’t go to QE, Trump will find a way to take control of the Fed:

Trump could purge members of the seven-strong Fed board one by one until they get the message. The law states that the president can terminate the 14-year term of a Fed governor “for cause”, usually meaning malfeasance or neglect.

But Trump has just abused his tariff powers on an heroic scale by invoking fictitious “emergencies”. He could no doubt stretch the meaning of “for cause” to anything he wants.

Since he has stretched the meaning of everything to the breaking point, causing numerous cases to rush toward the Supreme Court, I am sure he will not hesitate to stretch the meaning of “neglect” when it comes to ditching Fed members. I don’t care a fig about saving Fed members. I’m just saying expect big changes to come that move us toward monetizing the debt again, and then we’ll have to start looking at whether or not rising inflation could turn into hyperinflation, but I am not predicting, yet, that will happen. There are two many variables that have to work out first, but the collapse of the dollar does appear to be starting as nations flee Treasuries. So, on to that:

The Great Trump Dump in Treasuries

It is not that Trump wants Treasuries to dump, just the opposite; but that is clearly happening, regardless of what he wants:

There are a few reasons. One article points out that the world now has much more attractive safe-haven bonds available to it from places that only recently were seen as troubled, but they look good by comparison now:

Bond traders will be trying to gauge who blinks first, will it be the Fed or President Trump? If both stick to their current stance, every Treasury auction is a landmine which investors will fear stepping in to.

In the first rush for investment safe havens in years, US Treasury bonds are facing serious competition as a destination for global funds.

In Germany, the 10-year bund at 2.61% reflects the prospect of a flood of bond issuance as the government ramps up defense spending. Meanwhile, the rate on 10-year Japanese bonds has soared after spending years around zero and is now around 1.25% as ...

By those measures, though, US bonds just rapidly caught up, much surpassing the yields offered in Germany. However, that is because they have to because they are suddenly uncherished in a world that has no trade needs for them and in a world where hedge funds are having to rapidly deleverage from bond trades that are suddenly not profitable, forcing them to sell into a falling bond market (in terms of prices/values of the bonds they hold) because they have had to raise ready cash to cover their margin calls on failing stock bets.

Global bond markets were gripped by volatility on Wednesday, as the rollout of U.S. President Donald Trump’s reciprocal tariffs left investors scrambling to find safety in new areas — including German debt.

As Gundlach said, someone (big) is going to go broke. We’ll probably learn who that is the same way we learned about Bear Stearns and Lehman Bros … after it's done. This means, as for those whom I reported as saying about a week ago that a recession wasn’t near, WAKE UP!

“The idea that various of the administration’s policies could undermine foreign demand for Treasuries has been gaining currency,” said Matthew Raskin, head of US rates research at Deutsche Bank AG. It all adds up to a world where US exceptionalism no longer is the dominant theme, with potentially momentous long-term implications: Deutsche Bank warns of a “confidence crisis” in the dollar, while UBS Group AG sees a shot in the arm to the euro’s status as a global reserve currency.

You better believe it if this tariff war continues, and continuing is what is happening because, while I reported that Trump was lying through his teeth when he said that “China really wants to make a deal,” we got proof overnight of my claim: China is so NOT clamoring to make a deal that it just added 50 points to its own tariff rates but went much further than that and actually froze some select US companies completely out of its markets and also froze certain mineral sales to America completely, as I said it looked like they were getting read to do. The fight is fully engaged! China did not call Trump for a deal. China is armed for a long-term war. Trump was just flapping his lips.

It was always the height of folly to think China would capitulate. They never backed down from the last tariff war, and those tariffs (both US and Chinese) continued all the way to the present, and now China has raised them to 84% plus the freeze-outs of about a dozen major US corporations along the shutdown of vital mineral supplies. NO, China was not begging Trump for a deal! They’re squeezing him!

Europe has also stepped up its retaliatory tariffs. No one is backing down. Canada isn’t going to back down because Trump has made it clear that the cost of removing tariffs for Canada is that it ceases to be a nation!

This stuff is insane. It’s absolute imperialism for an ego so overblown that it has to control the world.

Capital flights are filling the skies

As the world now flees US Treasuries, here is the impact in just a couple of short days:

Chaos in the U.S. stock market has infected the bond market, fueling speculation about a potentially destabilizing shock to the global financial system….

The selloff in both stocks and bonds has been acute, pressuring liquidity in markets. "It's not at a crisis stage," said Robert Tipp, chief investment strategist at PGIM Fixed income, in a phone call Wednesday. But he said the jittery dynamics in markets were at risk of "spilling over" and overtaking Wall Street's ability to keep liquidity flowing through when investors need it most.

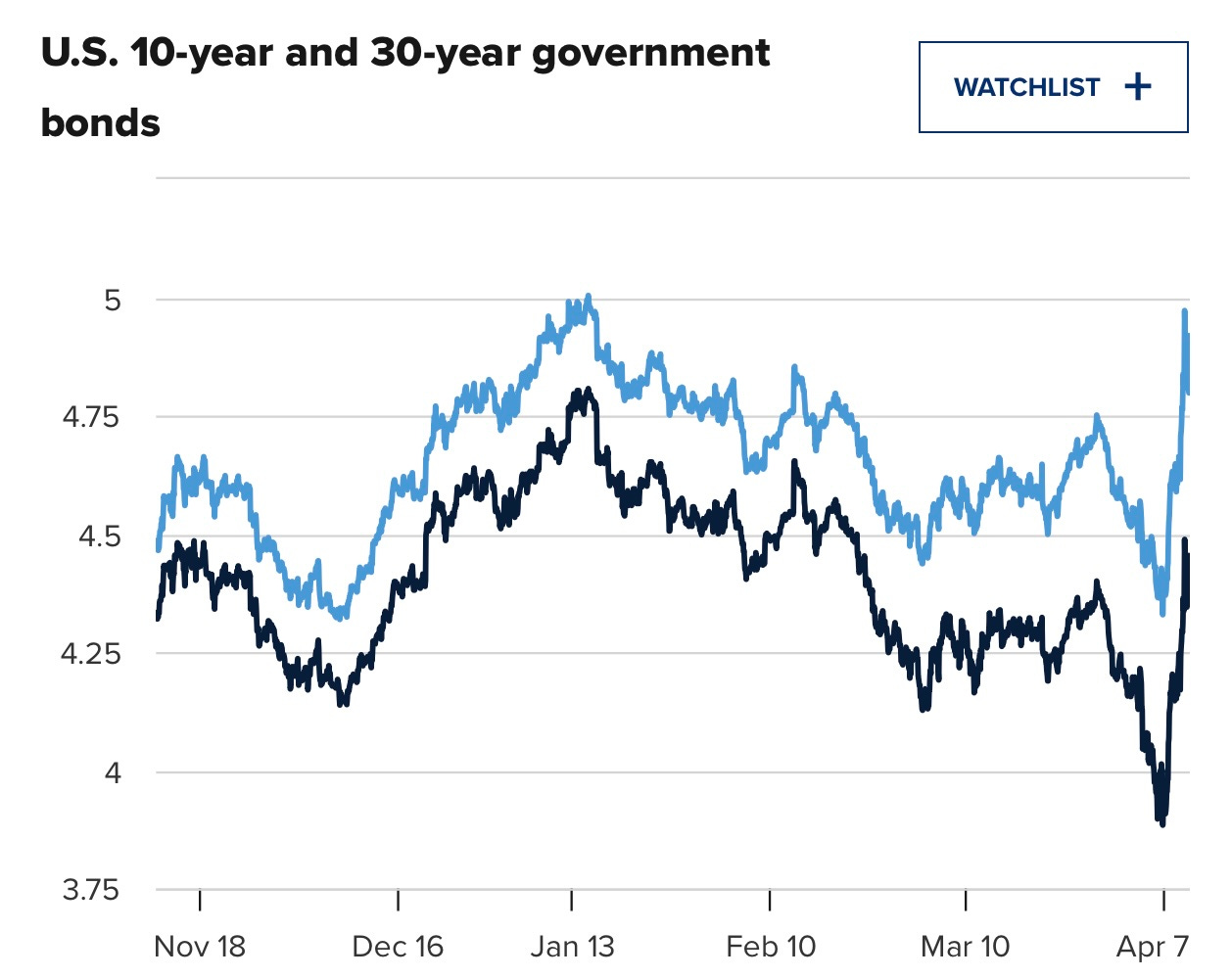

The iconic 10YR Treasury, on which so many US loans base their interest rates, just spiked above 4.5% mid-day, though it eased back down to just below 4.4%. However, only a week ago, it was at 3.9% due to capital from stocks seeking a safe haven. The 30YR hit an overnight high of 5.2%, a level not seen since the Fed tightening and QT in 2023.

However, in some hope that the floor hasn’t fallen out just yet, the latest bond auction at these higher yields saw ample bids, including from foreign investors because yields spiked enough overnight to draw some of them back. Not all auctions were rosy, however:

Tuesday’s $58 billion sale of 3-year notes offered some ominous signs. It produced a tail of 2.3 basis points in a sign of poor demand, and below-average bidding by non-dealers of 79.3%, which forced primary dealers to step in by more than they usually would. As Gillum put it, the 3-year Treasury auction “was objectively horrible, with the Treasury Department having to pay up to entice demand that still didn’t really show up.”

Those who jumped in when higher yields were offered may be foolish bets because tariffs have only just gone into play, and it will take a few months for the diminishment of trade to become seriously felt in the bond pits as trade dollars turn into an object of curiosity from the past. That is why I said above to wait until summer for this to get serious enough to drag the Fed back in kicking and screaming because it is still doing QT, albeit at a greatly diminished rate.

Treasurys can have ripple effects through global bond and currency markets. "You get no rest in markets," he said, when this kind of volatility hits Treasurys….

The unrelenting selling pressure has alarmed bond-market professionals, who are bracing for the threat of more knock-on effects, including the possibility, still somewhat remote, that global credit markets could seize up. Some, including Tom Simons, an economist at Jefferies, have said that liquidity conditions are starting to resemble the last major Treasury market meltdown in the spring of 2020.

Look at the long-term US Treasury bond action:

Those are spikes of historic size.

Hopeful auctions aside, here is the aerial 40,000-foot view of bond action:

U.S. Treasury Bonds Sell Off as 30-Year Yield Rises Most Since 1982

The selloff in U.S. government bonds gathered speed on Wednesday, with the 30-year Treasury yield set to rise the most in more than 40 years as a paradigm shift in trade policy upends the bond market….

Higher yields mean bond prices are declining, which isn’t typically what happens when stocks are selling off—investors generally buy U.S. Treasuries, considered the safest debt, in times of uncertainty. But despite the turmoil in the financial markets triggered by tariffs, Treasuries have been dumped, particularly those with long durations.

While the 30-year has taken the brunt of the damage, other maturities are getting hit as well. The 10-year yield … is on pace for its largest four-day gain since the 2008-09 financial crisis.

“Bond Markets In TROUBLE…. This is not what we signed up for,” wrote Andrew Brenner, head of international fixed income at NatAlliance Securities.

So, despite some hope in one of the auctions, the market is in turmoil, and some auctions did horribly. That’s what you get when big things are breaking—a lot of upheaval.

Speculation that a chunk of the selling is being conducted by foreign governments is rampant. Emerging market currencies are tumbling, pushing foreign central banks to sell Treasuries and use the dollar to buy their own currency to prop it up. The Japanese yen and the Canadian dollar are also down, as are most European currencies.

That indicates money in foreign markets moving out of US bonds.

Why would they want US Treasuries when …

-

They have little need of them for currency exchange on foreign trade anymore.

-

They have a great need to hurt the US as much as they can as quickly as they can in order to try to bring the tariff war to a close with some shock and awe of their own.

-

They need to rescue their own currencies because the whole global economy is rapidly melting away like a candle thrown into the fire.

-

As a result, they hate Trump and would love to maim him.

-

Many of them are sick of US hegemony, but all the more so now that the US is trying to take over the land masses of other nations and rename entire parts of the globe in its own arrogant make-America-great-again image.

-

Those nations that are faced with giving away their lands as the price of getting out of tariffs can never back away from the tariff war.

Hence, unsurprisingly,

The latest Treasury data … for January … showed that investors abroad have sold longer-term Treasuries for three consecutive months, with the latest move led by Canada.

Another explanation for the Treasury sales could be that U.S. assets are simply no longer preferred by foreigners given the country’s less than amicable relationship with its partners.

Of course. Who couldn’t see that result coming? Like I said, you may be able to bully them if you are the biggest, but you can’t stop them from hating your guts if you do. Bottom line: make yourself the trade enemy of all, and you start to smell bad, as people claim Trump’s body odor does, and then no one wants to be around you anymore. The US has become ugly to the point of hideous in the views of many foreigners.

China may be selling down its Treasury holdings before exchanging its U.S. dollars for gold, or for the currencies of countries with whom it has a less adversarial relationship (Europe? Japan? Commodity producers such as Australia and Canada?)…. “The fact that some of the biggest downside moves seem to be occurring during Asian hours might support this explanation.”

Again, of course! Indications in all these wild swings are consistent with nations ditching the dollar … likely for good once they make the shift. Who couldn’t see that coming from tariff wars at a time when other nations already distrust US hegemony? However, now we get to report it as an emerging fact, rather than a mere prediction. It is not easy to figure out on the fly exactly where the money is moving, but all paths seem to point in the direction of anywhere but the US. You can be sure China, having long wanted to reduce US hegemony, is putting all of its bets in that basket.

Other factors include the loss of liquidity from hedge funds unwinding their risky trading strategies. Exceptionally high uncertainty combined with expected higher inflation could also be leading investors to demand better returns. High gaps between U.S. revenue and spending have also penalized the U.S. Treasury market outlook….

Higher yields also mean President Donald Trump won’t be able to accomplish what he promised during the campaign. He won with the promise to lower the cost of goods and housing, and higher 10-year yields—on which mortgage, credit card, and other consumer rates are based—hamper that goal.

As another sign that nations are fleeing the dollar as the global trade currency like never before, consider Germany’s sudden keen interest in auditing its gold holdings at the Fed. Looks like they might be planning to move the gold out of US storage and closer to home because central banks DO use gold as a trade currency when they have to. Gold bars may now become the currency of choice since the BRICS nations have not come up with a currency to offer.

Germany’s government is discussing a very heavy but equally delicate problem: the possibility of getting 1,200 metric tonnes of its gold reserves out of the United States.

Countries don’t like to ship their gold if they can trust where it is located. Moving that many metric tons of gold can mean that it all winds up lost at sea, as has happened in many ill-fated shipments, whether due to a ship sinking or to pirates.

Some officials in the country are beginning to call for less trust and more verification.

Trust has been broken. Trump didn’t honor his last trade deals and has moved on from them to a full-on trade war. Therefore, trust will not be readily restored this time, and the one thing the dollar depends on for its global status, besides trade (now broken), has always been trust. When nations start looking at moving over a thousand tons of gold across the sea, you know trust is gone!

The Bundesbank and the German government must demonstrate foresight in this phase of global power shifts and immediately retrieve German gold from the USA. Especially at a time when Berlin and Brussels are discussing immense new debt, we need immediate access to all gold reserves in an emergency.

Of course, even Trump and Musk don’t trust that the gold is where the gold is supposed to be. They’ve been saying they want to personally inspect Fort Knox.

Sell America!

The Wall Street Journal writes that the market is in a “sell everything American” mode right now.

The sight of stocks, bonds and the currency all falling together would be a scary one for any emerging economy. It has now come to U.S. shores. While not yet a financial crisis, distressed selling is always a bad omen.

Late on Tuesday, Treasurys started rapidly selling off. The slump worsened overnight…. Several factors make this concerning, above all that the S&P 500 also tumbled as bonds headed lower, as did the U.S. dollar.

Welcome to the start of third-world America as we destroy ourselves out of our own arrogance. It’s becoming an everything-goes avalanche.

Of course, Trump is going to continue to do his best to jawbone markets, and greedy investors will likely listen for what they want to hear, as I argued; but the deeper reality of his tariff war is sinking in all around him (and us), regardless. Reality is the persistent force, not jawboning. While talk can ping market algorithms into bidding stock prices up, and Trump is good at doing that, the underlying reality is rapidly eroding away from the foundations of the US economy.

One thing that surprised Wall Street analysts about the initial reaction on April 3 was that the plunge in the stock market was mirrored by the greenback falling against most major currencies. This was a sign that foreign investors were losing faith that the U.S. economy would continue to outperform….

For the Treasury market in particular, a disorderly selling spree appears to be taking over from the initial measured caution.

Bombs away.

Speaking of which, Trump may soon need a good war to get attention in the press off his flailing tariff war. In times like this, real wars with real bombs have often been a popular choice for US presidents. So, that may up the pressure for war with Iran this weekend, as a couple of our other headlines below layout as being likely in the works.

Chaos sometimes goes in good directions, too

With all of that said, based on the week’s action and especially the overnight and morning fails in all markets, the stock and bond markets did some major flipping recently. The Dow shot higher than a 2,900-point absolutely historic climb, and two long-maturity Treasury auctions went rosy while another shorter-term Treasury failed horribly:

Bond-market participants got a major surprise Wednesday afternoon when the Treasury Department’s $39 billion auction of 10-year notes produced very strong demand, helping to alleviate concerns that buying interest would fail to hold up given tariff-driven volatility.

The fear going into the auction was that both foreign and domestic investors would pull back from the sale. Instead, results released just after 1 p.m. Eastern time showed indirect bidders took 87.9%, which was well above average, and that the sale produced a stop-through of 3 basis points in a sign of very solid demand.

I am inclined to attribute all of these contradictions in a 24-hour period to the manic gyrations of greed in a time of chaos. The scale of rallies we just saw is a phenomenon that is actually common in major bear markets after huge sell-offs—a major bull trap, where a huge relief rally comes in as the bulls muster all they can to buy back into what they suddenly see as huge bargains and try to force a bull market back into play, only to see those who get drawn back in slammed back down again … just as I said we would see with the help of the video clip from Once Upon a Time in Hollywood.

There is going to be some fierce head-banging from ceiling to floor and back to ceiling and back to floor again until the life gets smashed out of the bulls in a brutal battle.

The positive bond auctions likely occurred only because yields overnight spiked so astronomically upward that they did manage to attract buyers.

Even Powell seemed to have gone nuts, saying that inflation was now likely to be “persistent” to saying in one report that it is likely to fade this year.

Expect more floor-to-ceiling-to-floor head slamming in the weeks ahead. I think we are seeing tectonic moves in economics that are going to slam things around a lot. The land heaves up at one edge of the plate but sinks into the mantle at another. The caldera rises, blows out lava and smoke, and then collapses like a breathing, belching monster. These are the kinds of chaotic forces we are likely to see as the greatest economy on earth starts to crack and its molten interior starts to ooze.

Remember my maxim: There are no straight lines in economics; not for long anyway; so, after a straight line down for a day or two, you’re going to get a straight line back up. Big bear markets always have big bear rallies, also known as “bull traps” because of how they deceive investors back into the market with their sudden upward rush. Things as big as the entire US economy break in big moves … up and down … ceiling to floor, wall to wall, like in the previous video as investors get the snot pounded out of them.

(So MUCH is happening, and it’s so complicated, that is hard not to make each of my daily editorials a full Deeper Dive in terms of all they explore in depth. I’m going to try to dial that back, but there is a lot going on right now. I may take a break this weekend, since this week’s articles have been equal to Deeper Dives, by not writing one over the weekend, but that all depends on how much major action demands of me on Thursday, Friday, and over the weekend. Something tells me I’m not going to catch a break, especially with a major Middle East war—the one that has been feared the most for the longest—looking likely on the near event horizon as the headlines below also lay.)

About the author

David Haggith is the publisher/editor-in-chief of The Daily Doom.

Economic, Social and Political News of Our Troubled Times -- a non-partisan daily collection of the most consequential stories about our complex times from multiple sources around the world plus daily editorials like the one you read here.

Liked it? Take a second to support David Haggith by subscribing on Substack!