DID THE FED CAUSE THE 2008 RECESSION?

A review of the history regarding Fed interest rate policy yields information that says “yes”.

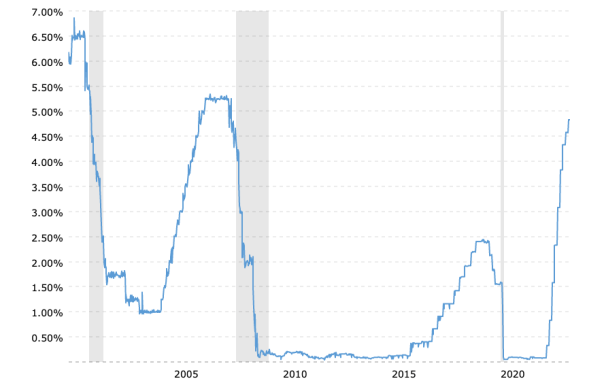

On June 30, 2004, the FOMC began to tighten policy by increasing the Fed Funds target rate to 1¼%. By June 2006, two years later, the target rate was at 6 1/4%. It remained at that level for the next year – well into 2007.

The tightening policy followed on the heels of one of the more aggressive moves in Fed history to lower interest rates in 2001-04. The decline in rates helped fuel a real estate price bubble which was encouraged by loose lending policies and ultra-low interest rates.

The chart below shows the history of the Fed Funds rate from 2000-2020…

FEDERAL FUNDS RATE – HISTORICAL CHART

As can be seen in the chart above, the Fed has embarked recently on a similar change in direction which has taken Fed Funds rate from near-zero to almost 5%, and higher than at any time since 2007 – just prior to the events which triggered the Great Recession.

FED’S ROLE IN THE GREAT DEPRESSION

The Fed’s ever-changing interest rate policy was in effect more than a century ago in the 1920s, too…

“Open market purchases in 1924 and 1927 provided plenty of cheap fuel for stock market investors and speculators. Liberal lending standards allowed margin loans of as much as ninety percent to ordinary retail stock investors. Speculation was rampant.

Beginning sometime in 1928, the Fed changed switched their emphasis to higher interest rates. The economy began to weaken and was slowing appreciably before the stock market crash in October 1929. A decade of economic depression followed.” (source)

ECONOMIC DISLOCATION IN 2008

As a result of higher interest rates and the temporary curtailment of cheap and easy credit, financial liquidity dried up. In essence, the effects of higher interest rates acted as a supply shock to the financial markets. A credit implosion triggered by a collapse in residential real estate followed by severe economic dislocation resulted. Housing starts declined by eighty percent (more supply shock) and unemployment soared from four and one-half percent to ten percent (demand shock).

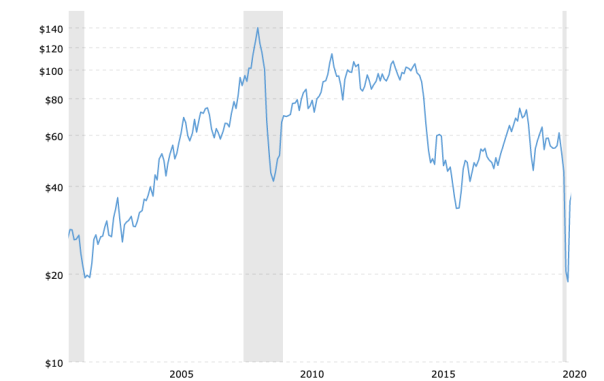

As if that were not bad enough, the economy experienced more supply shock as oil prices more than doubled in 2007-08. After dropping by two-thirds in the last six months of 2008, the price of crude oil more than doubled to exceed $100 a barrel again, and stayed at that level for several years.

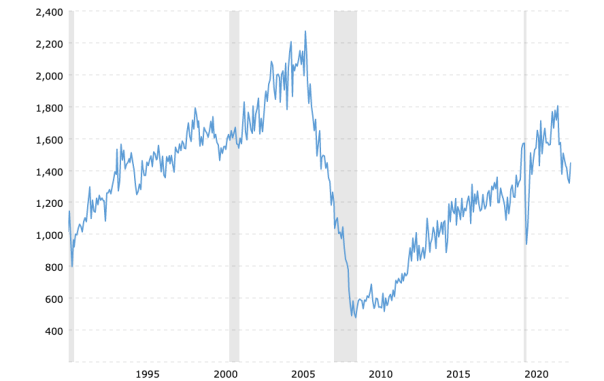

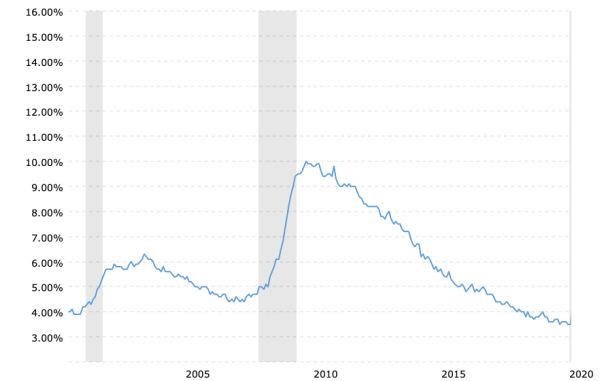

Below are charts (source) which illustrate the collapse in housing starts, the huge increase in the unemployment rate, and the extreme volatility in oil prices…

Housing Starts – Historical Chart

Unemployment Rate – Historical Chart

Crude Oil Prices – Historical Chart

FED RESPONSE

Fed response to the initial events at the onset of the Great Recession was swift and aggressive. The target interest rate went to near-zero almost immediately, and remained at or near that level for eight years. A half-hearted attempt to raise rates in 2016-17 was reversed and rates returned to near zero for five more years before the Fed’s latest attempt to move interest rates back to something more closely aligned with historic averages.

On the monetary front, the Federal Reserve entered the secondary market and gobbled up huge amounts of Treasury bonds and mortgage-backed securities (MBS).

The action was taken to stop an implosion in the credit markets resulting from falling real estate prices and reevaluation of credit quality.

Government did their best to help with a slew of new programs and regulations and financial support paid for with money created by the Fed and financed by taxpayers. There were bailouts on all fronts including banking, insurance, and securities. The names were previously considered stalwarts in the financial industry: Lehman Bros., Merrill Lynch, AIG, etc.

AFTER EFFECTS AND UNINTENDED CONSEQUENCES

The credit markets responded reasonably well to the Fed’s direct purchases of debt securities. It did not reverse the damage immediately, but it stopped the bloodletting. After several years, the bond market did recover and go to new heights of even more ridiculous proportion.

As far as lower interest rates, they seemed to not have the intended impact. The consumer, rather than spending pro-actively, seemed more intent on paying off debts, rather than incurring new obligations. Saving preempted spending.

The new money created sat in the coffers of the primary dealers and other banks as excess reserves. Having been bitten badly by the mortgage-lending bug and suffering from the effects of purging bad loans from their books, banks preferred to sit on the the money rather than lend it.

Consumers and small businesses obliged by changing their habits as well. Too many of them were dealing with the collateral damage created by the huge drop in housing prices.

In addition, new credit standards excluded large segments of the population who had previously been eager to “borrow and spend” and did.

Recovery was a slow and laborious process. Experts and others questioned why the intended effects weren’t showing up in the economy, which labored along at a perilously slow rate.

Where was all of that “new” money going? It went into stocks, bonds, and real estate. Fed money fueled another bubble of spectacular size in financial assets and house prices.

THE FED’S LATEST DILEMMA

The bubble continued to grow until the Fed changed their interest rate policy early last year. Since then, asset prices have come down substantially and recovered somewhat. More importantly, the economy has slowed measurably.

Auto and light truck sales are down, and so are housing starts. The sharp rise in retail sales post-Covid was stopped in its tracks with the onset of higher interest rates.

Financially speaking, stocks, bonds, and commodities are all appreciably lower.

Right now things appear to be on hold pending the next Fed rate decision. Will it stop pursuing a tight money policy; or will it continue raising rates?

Continuing with the current policy of higher interest rates might lead to further financial and economic problems similar to what happened in 2008 (Great Recession) and 1929 (Great Depression).

Purposely pursuing lower interest rates could trigger renewed weakness for the U.S. dollar and accelerate the effects of inflation.

The Fed has a history of changing interest rate policy abruptly. Eventually, they will change direction again. That change in policy might not come, though, until after another financial and economic collapse. (see A Depression For The 21st Century and Fed Is Chasing Its Own Tail)

Kelsey Williams is the author of two books: INFLATION, WHAT IT IS, WHAT IT ISN’T, AND WHO’S RESPONSIBLE FOR IT and ALL HAIL THE FED!

About the author

Analyst, Author, and Owner of Kelsey's Gold Facts

Kelsey Williams has more than forty years experience in the financial services industry, including fourteen years as a full-service financial planner. His website, Kelsey's Gold Facts, contains self-authored articles written for the purpose of educating and informing others about gold within a historical context. In addition to gold, he writes about inflation and the Federal Reserve.

Kelsey is the author of two books: INFLATION, WHAT IT IS, WHAT IT ISN'T, AND WHO'S RESPONSIBLE FOR IT and ALL HAIL THE FED!

Kelsey Williams is available for private consultations, public speaking, and interviews at kwilliams@kelseywilliamsgold.com