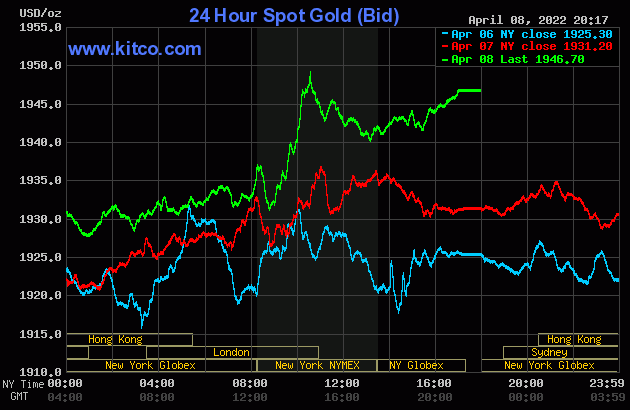

The gold price wandered quietly lower in the Far East on their Friday morning -- and the low tick of the day was set around 1 p.m. China Standard Time on their Friday afternoon. It then wandered quietly higher from there until about five minutes before the COMEX open -- and was then sold lower until 8:45 a.m. EDT. The ensuing rally was capped minutes after 10 a.m. in New York, which may or may not have coincided with the afternoon gold fix in London. It was sold quietly lower from that point until around 1:10 p.m. -- and then crawled quietly higher until the market closed at 5:00 p.m. EDT.

The low and high ticks in gold were reported as $1,930.40 and $1,952.20 in the June contract. The April/June price spread differential in gold at the close yesterday was $4.00...June/August was $6.60...August/October was $6.40 -- and October/December was $7.60 an ounce.

Gold was closed in New York on Friday afternoon at $1,946.70 spot, up $15.50 from Thursday. Net volume was very light at 129,500 contracts -- and there was a bit under 14,500 contracts worth of roll-over/switch volume on top of that...mostly into August and December.

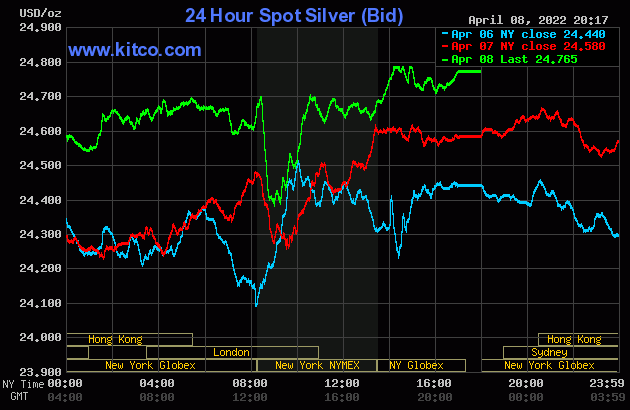

Silver's price path was mostly similar gold's in GLOBEX trading...but only up until a minute or so before 8:30 a.m. in New York. It was then hammered lower, with its low tick coming at exactly 9:00 a.m. EDT. Its ensuing rally was capped at the same moment as gold's -- and from that juncture it wandered very quietly lower until 1:10 p.m. At that point it made another bolt for freedom, but ran into a brick ceiling at $24.79 spot around 2:10 p.m. EDT. A quiet down/up move followed for the remainder of the after-hours trading session.

The low and high ticks in silver were recorded by the CME Group as $24.495 and $24.935 in the May contract. The May/July price spread differential in silver at the close in New York yesterday was 8.5 cents...July/September was 8.8 cents... September/December 14.0 cents an ounce.

Silver was closed on Friday afternoon in New York at $24.765 spot, up 18.5 cents from Thursday. Net volume was very much on the lighter side at 34,500 contracts -- and there was around 19,700 contracts worth of roll-over/switch volume in this precious metal...mostly into July, with a bit into September.

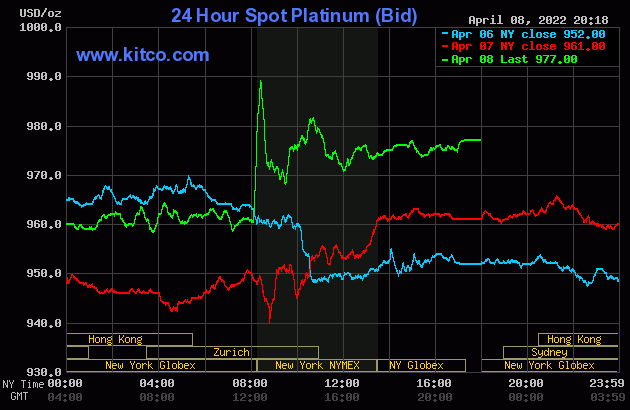

Platinum wandered/chopped very quietly sideways throughout all of the GLOBEX trading session overseas -- and that ended with a bang minutes after 2 p.m. in Zurich/8 a.m. in New York when this LPPM news hit the wires. The price went near vertical, but 'da boyz' stepped in about thirty minutes later to cap that rally -- and then drive it lower. That sell-off lasted until around 9:35 a.m. EDT -- and its ensuing rally ran into the same fate -- and its price was returned to 'trend' at exactly noon in New York. It was allowed to crawl a bit higher until trading ended at 5:00 p.m. Platinum was closed at $977 spot, up 16 bucks on the day -- and 22 dollars off its Kitco-recorded high tick.

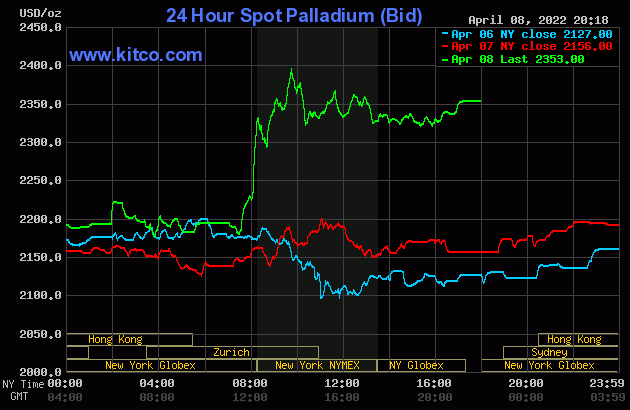

Palladium rallied to around the $2,200 spot mark by around 10 a.m. China Standard Time on their Friday morning -- and then traded rather unevenly sideways to a bit lower until around 1:30 p.m. in Zurich. It began to head sharply higher from there -- and then piggy-backed on the same LPPM news starting minutes after 2 p.m. CEST/8 a.m. EDT. The Big 4/8 shorts finally got the price capped around 9:45 a.m. during the COMEX trading session in New York -- and it was sold lower until around 10:20 a.m. EDT. >From that juncture it was forced to chop/wander quietly sideways until trading ended at 5:00 p.m. Palladium was closed at $2,353 spot, up $197 on the day -- and 42 dollars off its Kitco-recorded high tick.

Based on the kitco.com spot closing prices in silver and gold posted above, the gold/silver ratio worked out to 78.6 to 1 on Friday...unchanged from Thursday.

And here's Nick Laird's 1-year Gold/Silver Ratio chart, updated with this week's data. Click to enlarge.

![]()

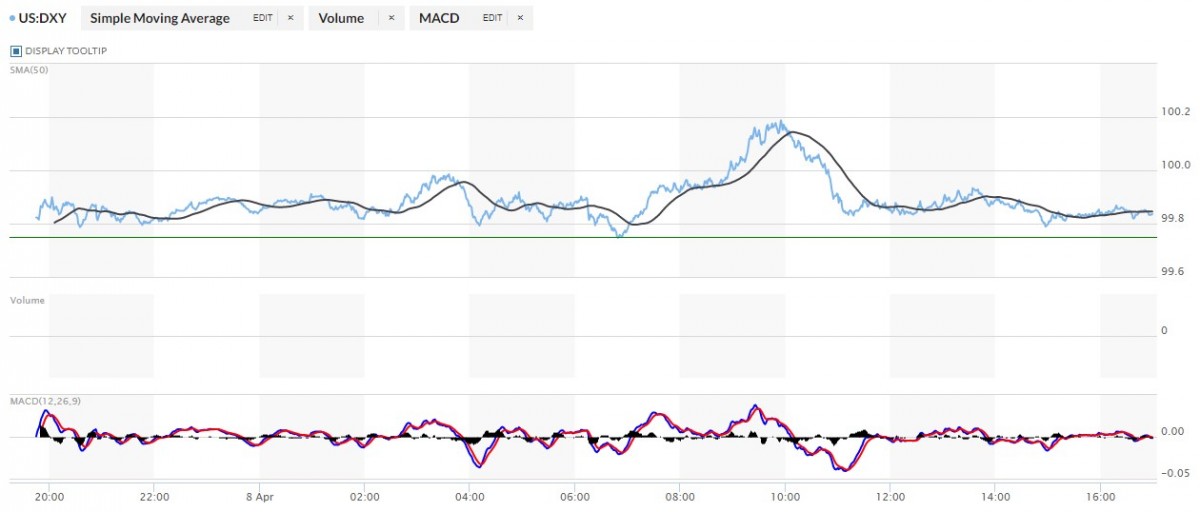

The dollar index closed very late on Thursday afternoon in New York at 99.75 -- and then opened higher by 7 basis points once trading commenced at 7:45 p.m. EDT on Thursday evening, which was 7:45 a.m. China Standard Time on their Friday morning. It rallied a bit from there over the next fifteen minutes or so -- and then proceeded to wander quietly sideways to a bit lower until around 11:50 a.m. in London. Its ensuing rally topped out at 9:55 a.m. in New York -- and it was then sold quietly lower until around 11:12 a.m. EDT. It then wandered quietly sideways from that juncture until the market closed at 5:00 p.m.

The dollar index finished the Friday trading session at 99.84...up 9 basis points from its close on Thursday.

Here's the DXY chart for Friday, thanks to marketwatch.com. Click to enlarge.

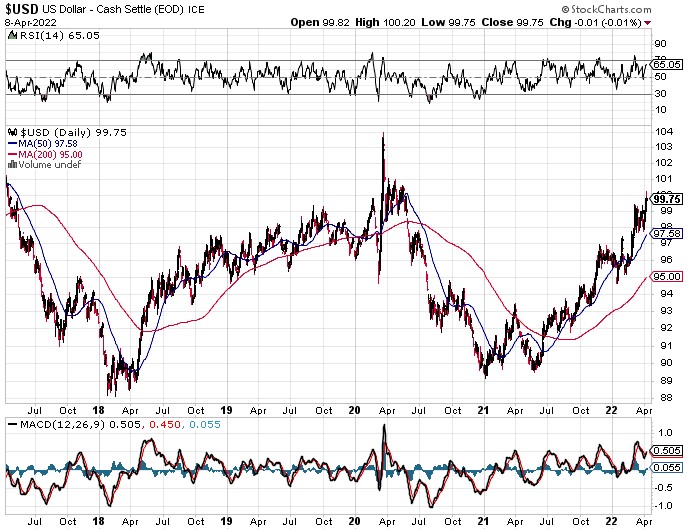

And here's the 5-year U.S. dollar index chart that appears in this spot in every Saturday column, courtesy of stockcharts.com as always. The delta between its close...99.75...and the close on the DXY chart above, was about 9 basis points below its spot close on the DXY chart above. Click to enlarge.

One again there was zero correlation between the currencies and what was happening with regards to precious metal prices.

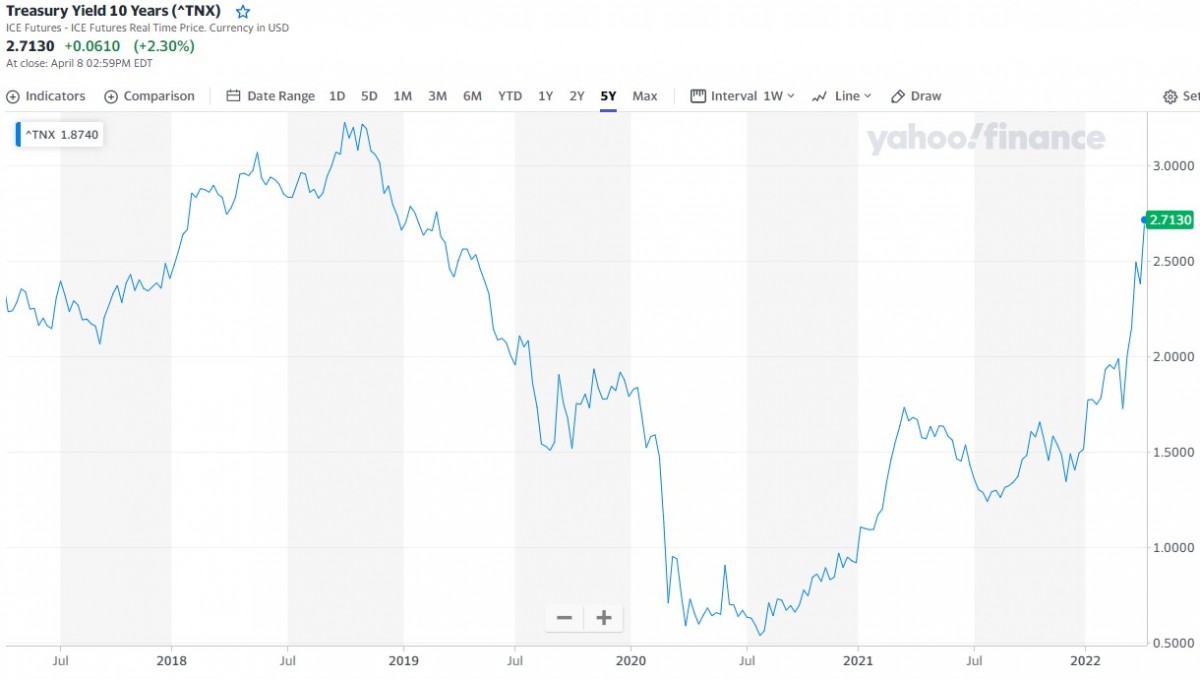

U.S. 10-Year Treasury: 2.7130%...up 0.0610 (+2.30%)...as of 02:59 p.m. EDT

Here's the 5-year 10-year U.S. Treasury chart from the yahoo.com Internet site -- and it puts the yield curve into a somewhat longer-term perspective. Click to enlarge.

As you are more than aware, the only reason that yields are where they are, is because the central banks of the world continue to buy up virtually all, if not all of the sovereign debt being issued. That isn't about to stop anytime soon, as Japan just announced very recently -- and the European Central Bank was in a snit about yesterday in this Zero Hedge article from Richard Saler linked here.

As the saying goes "bonds are guaranteed certificates of confiscation" -- and that fact is now on full display in all the bond markets of the world. The Fed says it's going to be unwinding its balance sheet -- and the obvious question on everyone's lips is..."who's going to buy them?"

![]()

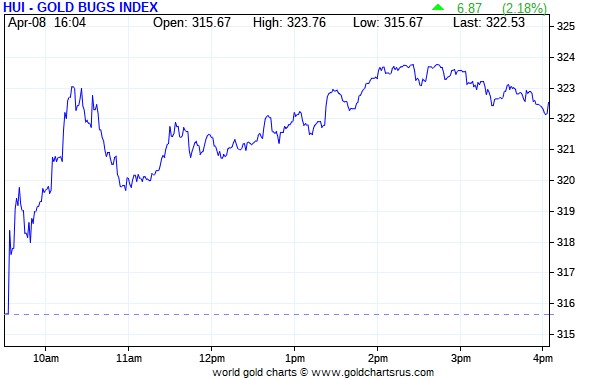

The gold shares began to head higher right from the moment that trading began at 9:30 a.m. in New York on Friday morning -- and that lasted until around 10:20 a.m. EDT. They were then sold a bit lower until a few minutes before 11 a.m. They began to creep higher from there, with their respective highs coming around 2:25 p.m. EDT. They were sold a bit lower until the market closed at 4:00 p.m. The HUI finished up 2.18 percent.

Computed manually, Nick Laird's Intraday Silver Sentiment/Silver 7 Index closed up 2.69 percent.

And here's Nick's 3-year Silver Sentiment/Silver 7 Index chart, updated with Friday's candle. Click to enlarge.

The star yesterday was SSR Mining, as it closed higher by 4.20 percent -- and the biggest underperformer was Peñoles, as it closed up only 1.14 percent on 7,600 shares traded.

The latest silver eye candy from the reddit.com/Wallstreetsilver crowd is linked here.

![]()

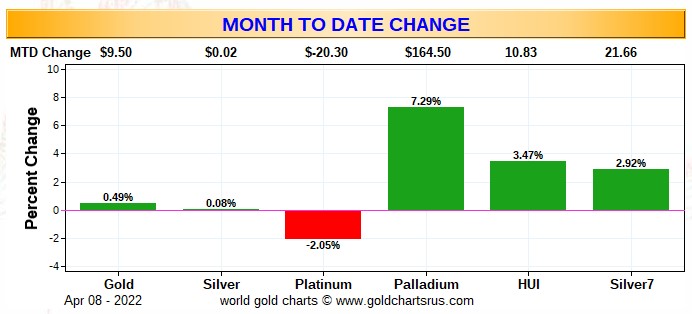

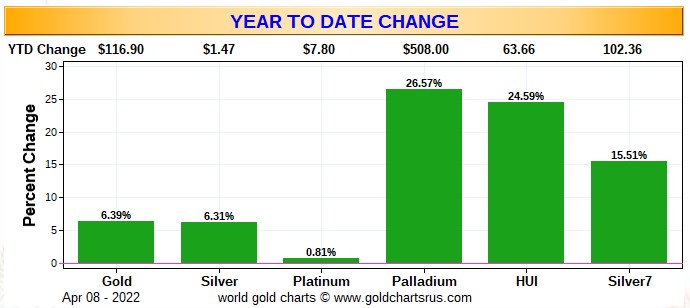

Here are two of the three usual charts that show up in every weekend missive. They show the changes in gold, silver, platinum and palladium in both percent and dollar and cents terms, as of their Friday closes in New York — along with the changes in the HUI and the Silver 7 Index.

Here's the month-to-date chart...and it's green across the board, except for platinum. The Silver 7 Index would be doing a little better if Peñoles wasn't part of it, but there's nothing that can be done about that. Click to enlarge.

Here's the year-to-date chart -- and it's still wall-to-wall green...with the silver stocks being the underperformers vs. its underlying precious metal so far this year. That will obviously change at some point. Palladium's gain year-to-date is impressive...but obviously down a very considerable amount because of the pounding it has taken during the last month. It would have been down even more, except for its strong rally yesterday -- and platinum got saved for the same reason. Click to enlarge.

Of course how much more in the way of gains were going to see going forward continues to be in the hands of the commercial traders of whatever stripe, as they alone control the price of everything precious metals-related...until they don't.

![]()

The CME Daily Delivery Report for Day 8 of April deliveries showed that 62 gold and 11 silver contracts were posted for delivery within the COMEX-approved depositories on Tuesday.

In gold, there were five short/issuers in total -- and the three biggest were Japanese trading house Mizuho, Goldman Sachs and Morgan Stanley, with 28, 15 and 15 contracts out of their respective client accounts. There were eight long/stoppers in total -- and the three largest there were JPMorgan and British bank Barclays, picking up 25 and 11 contracts for their respective client accounts... followed by Citigroup, stopping 11 contracts for their house account.

In silver, the only short/issuer was Morgan Stanley -- and the two long/stoppers were JPMorgan and ADM, as they picked up 8 and 3 contracts. All contracts, both issued and stopped, involved their respective client accounts.

In platinum, there were 44 contracts issued and stopped.

The link to yesterday's Issuers and Stoppers Report is here.

Month-to-date there have been 23,941 gold contracts issued/reissued and stopped -- and in silver that number is now up to 999 COMEX contracts. In platinum, there have been 2,248 COMEX contracts issued and stopped so far in April. In palladium, there have been 2 contracts issued and stopped.

The CME Preliminary Report for the Friday trading session showed that gold open interest in April dropped by 20 contracts, leaving 2,046 still open, minus the 62 contracts mentioned a bunch of paragraphs ago. Thursday's Daily Delivery Report showed that 64 gold contracts were actually posted for delivery today, so that means that 64-20=44 more gold contracts just got added to the April delivery month. Silver o.i. in April declined by 119 COMEX contracts, leaving only 102 still around, minus the 11 contracts mentioned a bunch of paragraphs ago. Thursday's Daily Delivery Report showed that 132 silver contracts were actually posted for delivery on Monday, so that means that 132-119=13 more silver contracts were added to April deliveries.

Total gold open interest at the close on Friday rose by 10,139 COMEX contracts -- and total silver o.i. increased by 4,607 contracts...not unexpected...with both numbers subject to some revision by the time the final figures are posted on the CME's website on Monday morning CDT.

There was a deposit in GLD yesterday, as an authorized participant added 102,643 troy ounces of gold -- and there was also 35,762 troy ounces of gold added to GLDM. There were no reported changes in SLV.

In other gold and silver ETFs and mutual funds on Planet Earth on Friday, net of any changes in COMEX, GLD, GLDM & SLV inventories, there was a net 47,954 troy ounces of gold removed, but a net 75,979 troy ounces of silver was added.

There was no sales report from the U.S. Mint yesterday.

Month-to-date the mint has sold 26,000 troy ounces of gold eagles -- 7,000 one-ounce 24k gold buffaloes -- and only 425,000 silver eagles.

And still no Q4/2021 or 2021 Annual Report from the Royal Canadian Mint. I don't remember them being this late before -- and we're already into Q2/2022.

There was very little activity in gold over at the COMEX-approved depositories on the U.S. east coast on Thursday. There was 5,690.727 troy ounces/177 kilobars received -- and every kilobar of that amount ended up at Manfra, Tordella & Brookes, Inc. There was 14,950.224 troy ounces/465 kilobars shipped out...250 from the International Depository Services of Delaware...200 from Brink's, Inc. -- and the remaining 15 kilobars departed Manfra, Tordella & Brookes, Inc.

There was a bit of paper activity, as 25,648 troy ounces was transferred from the Eligible category and into Registered over at Brink's, Inc...no doubt scheduled for delivery in April sometime. The remaining 192.900 troy ounces/8 kilobars was transferred from the Registered category and back into Eligible over at Manfra, Tordella & Brookes, Inc.

The link to the above COMEX gold activity on Thursday is here.

It was another pretty busy day in silver, as one rather small truckload...542,787 troy ounces...was dropped off at JPMorgan -- and that was all the 'in' activity there was. There was 1,176,383 troy ounces shipped out.

In the 'out' category, there were six different depositories involved. The largest amount was the 599,005 troy ounces/one truckload that departed JPMorgan. In second and third place were the 289,004 and 177,291 troy ounces that got shipped out of Brink's, Inc. and HSBC USA respectively.

There was a bit of paper activity, as 313,212 troy ounces was transferred from the Registered category and back into Eligible -- and that took place over at JPMorgan.

The link to all of Thursday's COMEX activity in silver, is here.

The only activity in gold over at the COMEX-approved gold kilobar depositories in Hong Kong on their Thursday was the 170 kilobars that got shipped out of Loomis International. The link to that, in troy ounces, is here.

![]()

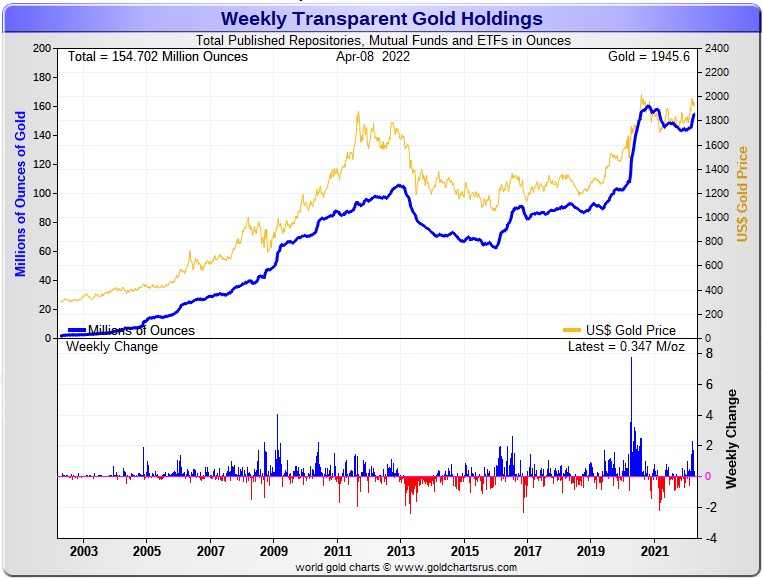

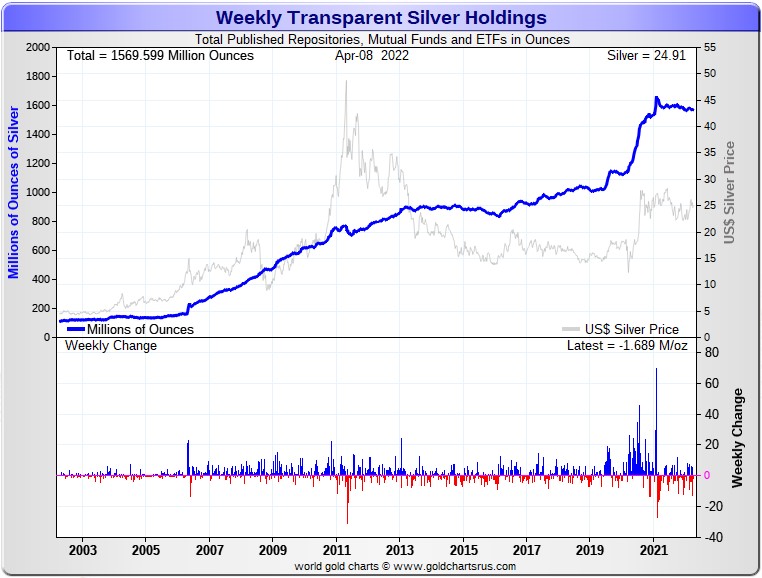

Here are the usual two 20-year charts that show up in this space every Saturday. They show the total amount of physical gold and silver held in all know depositories, ETFs and mutual funds as of the close of business on Friday.

During the week just past, there was a net 347,000 troy ounces of gold added -- and a net 1,689,000 troy ounces of silver was removed. Click to enlarge.

Ted is of the opinion that any and all silver that's required by SLV is being provided by JPMorgan and Friends, rather than allowing the short position to blow out to alarming levels. He also assumes that they're supplying all the other silver ETFs and mutual funds that require physical silver as well.

I'll be more than interested in what the next short report shows on 11 May...which is Monday.

The physical shortage in silver continues to creep along -- and the fact that JPMorgan has been issuing silver contracts out of their house account in both March and April...not to mention the physical silver being provided to all and sundry mentioned above...shows how extreme the situation has become.

Retail silver demand continues to be white hot as far as I can tell -- and delivery times for product from the various sovereign and private mints is still many weeks to months for a lot of bread and butter items.

![]()

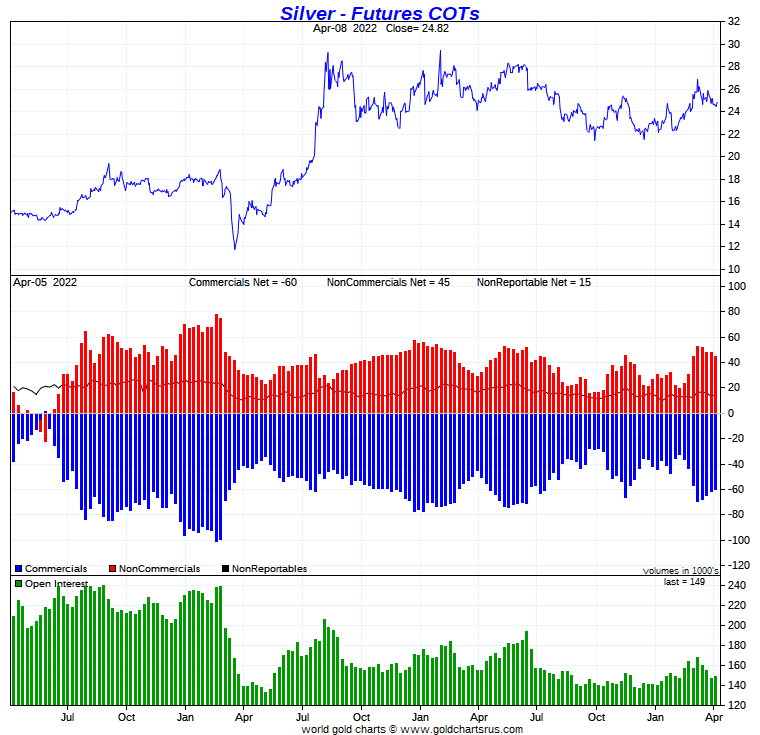

The Commitment of Traders Report, for positions held at the close of COMEX trading on Tuesday, showed smallish improvements in the commercial net short positions in both gold and silver.

In silver, the Commercial net short position decreased by 1,336 COMEX contracts, or 6.7 million troy ounces -- and that improvement came as a result of Ted's raptors adding to their long positions, as the Big 8 shorts did next to nothing on a net basis.

The commercial traders arrived at that number by increasing their long position by 1,333 COMEX contracts -- and reduced their short position by 3 contracts. It's the sum of those two numbers that represents their change for the reporting week.

Under the hood in the Disaggregated COT Report, it was all Managed Money trader selling -- and then some, that accounted for the change, as they decreased their net long position by 3,166 contracts. The Other Reportables were also sellers during the reporting week, but only 40 contracts worth, which was hardly worth calculating. On the other hand, the Nonreportable/small traders were big buyers, as they increased their net long position by 1,870 COMEX contracts.

Doing the math: 2,896 plus 40 minus 1,870 equals 1,336 COMEX contracts, the change in the Commercial net short position.

The Commercial net short position in silver now sits at 300.2 million troy ounces...down 6.7 million troy ounces from the 306.9 million troy ounces that they were short in last Friday's COT Report...which is obviously the headline number change mentioned further up.

The Big 8 are short 369.8 million troy ounces in this week's COT Report, a decrease of only 100,000 troy ounces from the 369.9 million troy ounces they were short in last Friday's COT Report.

The headline change in the Commercial net short position above showed an decrease of 6.7 million troy ounces. So Ted's raptors, the small commercial traders other than the Big 8 shorts did virtually allof the buying during the reporting week...to the tune of 6.7-0.1=6.6 million troy ounces...1,320 COMEX contracts...as they increased their long position by that amount.

It was their buying of long positions that had the mathematical effect of decreasing the commercial net short position by the amount that it did...except for that net 100,000 troy ounces bought by the Big 8 shorts.

Always remember that despite their small size, Ted's raptors are still commercial traders in the commercial category.

The Big 8 are short 369.8/300.2 equals about 123 percent of the Commercial net short position in silver, up from the 121 percent they were short in last week's COT Report -- and all because of all the longs purchased by Ted's raptors.

Here's the 3-year COT chart for silver, courtesy of Nick Laird as always. Click to enlarge.

This insignificant decrease in the Commercial net short position in silver, although welcomed, still leaves the futures market structure in silver very much on the bearish side...especially from a Big 4/8 short perspective. So nothing has changed from last week's COT Report.

However, however tiny the amount, this is the first week of the last three, that the Big 4/8 have decreased their net short position in silver...as it's been an all-raptor affair.

Ted is still of the opinion that there's a 'whale' in the Swap Dealer category that holds a long position of at least 15,000 contracts. That trader has held that position for many months now. What it means, Ted's not sure about...but it certainly isn't bearish for the price.

The commercial traders in silver are still in a position to lay a beating on the silver price going forward -- and Ted's of the opinion that it will take a price of under $23/ounce to do a proper clean out.

But can they or will they, is a question that still remains unanswered as of this writing -- and events of this past month have most likely changed a lot of things.

And to repeat Ted Butler's quote from last Friday's column..."[O]ne of these days, market structure considerations, as defined by readings in the Commitments of Traders (COT) report, will matter little – supplanted by physical market considerations or other things (like the OTC derivatives positions of the banks.)"

Whether we've reached that point, is yet another question that remains unanswered, but it's a given that the current situation can't continue forever, especially considering the near insatiable demand for physical silver at both the wholesale and retail levels.

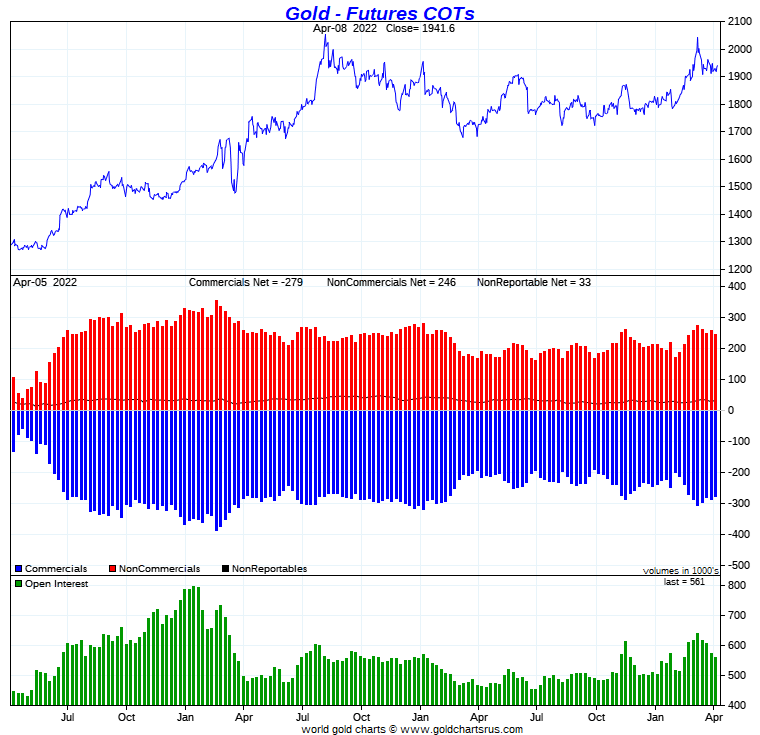

In gold, the commercial net short position declined by 7,179 COMEX contracts, or 717,900 troy ounces of the stuff...0.72 million troy ounces.

They arrived at that number by reducing their long position by 8,544 COMEX contracts, but also reduced their short position by 15,723 contracts -- and it's the difference between those two numbers that represents their change for the reporting week.

Under the hood in the Disaggregated COT Report, both the Managed Money and Other Reportables were the big sellers. The former category reduced their net long position by 6,675 COMEX contracts...mostly by adding to their gross short position -- and the latter category by 5,380 contracts...mostly by reducing their gross long position.

Once again -- and like in silver, it was the Nonreportable/small traders that were the big buyers, as they increased their net long position by a hefty 4,876 COMEX contracts.

Doing the math: 6,675 plus 5,380 minus 4,876 equals 7,179 COMEX contracts, the change in the commercial net short position.

The commercial net short position in gold now sits at 27.88 million troy ounces, down 710,000 troy ounces [0.71 million] from the 28.59 million troy ounces they were short in last Friday's COT Report...which is obviously the change in the headline number further up...with the minor difference being a rounding error.

The short position of the Big 8 traders is now 26.97 million troy ounces, up 0.08 million troy ounces from the 26.89 million troy ounces they were short in last week's COT Report.

But since the headline change in the commercial net short position showed an decrease of 717,900 troy ounce/0.72 million troy ounces rounded up, it means that Ted's raptors, the small commercial traders other than the Big 8, decreased their own short position by 0.72+0.08=0.80 million troy ounces/8,000 COMEX contracts to make up the difference -- and that's what they did.

Their buying of long contracts/covering short positions had the mathematical effect of decreasing the commercial net short position by that amount.

As in silver, don't forget that despite their small size, Ted's raptors are still commercial traders in the commercial category -- and it was yet another all raptor affair this week.

From the above numbers, the Big 8 traders are short 26.97/27.88 equals about 97 percent of the commercial net short position in gold...down about 3 percentage points from the approximately 94 percent they were short in last Friday's COT Report.

This means that Ted's raptors, the small commercial traders other than the Big 8, hold the remaining 3 percent of the commercial net short position in gold -- and are that far away from being net long gold.

Here's Nick Laird's 3-year COT chart for gold, updated with Friday's data. Click to enlarge.

Ted said that the gold 'whale' in the Other Reportables category...which he believes is John Paulson...is still there -- and appears that he took delivery of about 5,000 contracts worth of gold during April, so he remains long gold by about 35,000 contracts in the COMEX futures market...down from the 40,000 Ted reported last week.

Like last week's COT Report the Big 4 reduced their short position during the current reporting week, while the Big '5 through 8' increased their net short position during the same period...which was something that Ted mentioned on the phone again yesterday afternoon.

So, like in silver, the set-up in the COMEX futures market still remains very bearish.

Ted feels that it would take an engineered price decline in gold down to about $1,800 to clean out all the longs that have been added in the last month or so -- and [like in silver] whether or not that is even possible in the current monetary, financial and political environment remains to be seen.

Gold's 50 and 200-day moving averages still remain unbroken to the downside -- and whether that matters this time or not, also remains to be seen.

And to repeat Ted's quote from the COT commentary on silver above..."[O]ne of these days, market structure considerations, as defined by readings in the Commitments of Traders (COT) report, will matter little – supplanted by physical market considerations or other things (like the OTC derivatives positions of the banks.)"

So we wait some more.

In the other metals, the Managed Money traders in palladium increased their net long position by 63 COMEX contracts -- and are still net short palladium by 324 contracts. In platinum, the Managed Money traders decreased their net long position by a further 3,316 contracts during the reporting week -- but are still net long the COMEX futures market by 5,360 COMEX contracts...about 9 percent of total open interest, down about 5 percentage points from last week. The Producer/Merchant category continues to be mega net short against all others in platinum...including the Swap Dealers in the commercial category. In copper, the Managed Money traders decreased their net long position by an insignificant 140 COMEX contracts -- and are net long copper by 40,554 COMEX contracts at the moment...about 1.01 billion pounds of the stuff -- and about 19 percent of total open interest...down about 1 percentage point from what they were net long in last Friday's COT Report.

![]()

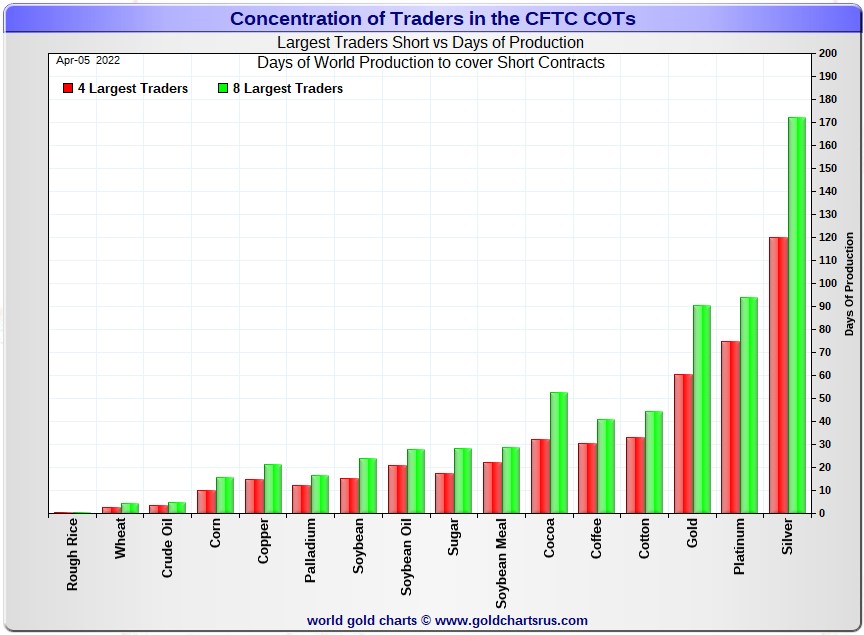

Here’s Nick Laird’s “Days to Cover” chart, updated with the COT data for positions held at the close of COMEX trading on Tuesday, April 5. It shows the days of world production that it would take to cover the short positions of the Big 4 — and Big '5 through 8' traders in each physically traded commodity on the COMEX.

I consider this to be the most important chart that shows up in the COT series -- and it always deserves a minute of your time. Click to enlarge.

In this week's 'Days to Cover' chart, the Big 4 traders are short about 120 days of world silver production, down about 1 day from last week's COT Report. The ‘5 through 8’ large traders are short an additional 52 days of world silver production, up about 1 day from last Friday's report, for a total of about 172 days that the Big 8 are short -- unchanged from last week's COT Report.

That 172 days that the Big 8 are short, represents almost six months of world silver production, or 369.8 million troy ounces of paper silver held short by the Big 8 commercial traders.

In the COT Report above, the Commercial net short position in silver was reported by the CME Group at 300.2 million troy ounces. As mentioned in the previous paragraph, the short position of the Big 4/8 traders is 369.8 million troy ounces. So the short position of the Big 4/8 traders is larger than the Commercial net short position by 369.8-300.2=69.6 million troy ounces...up 6.6 million troy ounces from last week's COT Report...1,320 COMEX contracts...the number of long contracts bought by Ted's raptors during the past reporting week.

The reason for the difference in those numbers is that Ted's raptors, the small commercial traders other than the Big 8, are net long silver by that amount...69.6 million troy ounces/13,920 COMEX contracts.

As per the first paragraph above, the Big 4 traders in silver are short around 120 days of world silver production in total. That's 30 days of world silver production each, on average...down a tiny amount from last Friday's report. The traders in the '5 through 8' category are short 52 days of world silver production in total...13 days of world silver production each on average -- up a small amount from last week's COT Report.

The Big 8 traders are short 49.8 percent of the entire open interest in silver in the COMEX futures market, which is down a tiny bit from the 50.2 percent they were short in the last COT report. And once whatever market-neutral spread trades are subtracted out, that percentage would certainly be over the 55 percent mark. In gold, it's 48.1 percent of the total COMEX open interest that the Big 8 are short, up a bit from the 46.8 percent they were short in last Friday's COT Report -- and close to the 55 percent mark once their market-neutral spread trades are subtracted out.

In gold, the Big 4 are short 60 days of world gold production, down about 1 day from last Friday's COT Report. The '5 through 8' are short 30 days of world production, up 1 day from last week...for a total of 90 days of world gold production held short by the Big 8 -- unchanged from last Friday's COT Report -- and the week before. Based on these numbers, the Big 4 in gold hold about 67 percent of the total short position held by the Big 8...down about 1 percentage point from last Friday's COT Report.

The "concentrated short position within a concentrated short position" in silver, platinum and palladium held by the Big 4 commercial traders are about 70, 80 and 75 percent respectively of the short positions held by the Big 8...the red and green bars on the above chart. Silver is about unchanged from last week...platinum is also about unchanged from a week ago -- and palladium is up about 6 percentage points week-over-week.

Nothing has changed. The Big 4/8 traders are still very firmly stuck on the short side in both gold and silver -- and they increased their short position in gold during the reporting week -- and decreased it in silver by an immaterial amount.

As I keep pointing out -- and will mention again, the Big 4/8 shorts will never be able to extricate themselves fully from the short side, if that was ever their intent...particularly the Big 4. At some point they're going to have eat the lion's share of the short positions that they currently hold. The only way that they can do that is to go into the market and buy longs...or deliver physical metal, but only if the long holders are in a position to accept delivery. Ted says that a lot of them aren't.

So unless the powers-that-be at the CFTC and CME Group have something nefarious up their sleeves, or they're bailed out by the likes of the Exchange Stabilization Fund, the U.S. Treasury or the Fed, their potential loses can only be imagined...think LME nickel times 100 or more. But I very much doubt that it will be allowed to happen, especially for the 'too big to fail' bullion banks in the Big 4 category.

What happened on the LME involving the nickel market will most likely be a template for what will occur over at the CME Group at some point, as they rush to protect the big shorts on any runaway price activity to the upside, as that's their primary function.

But as of this moment, there are no upside daily limits as to how high gold and silver prices can rise in the COMEX futures market.

However, the circumstances in silver have been altered by an unimaginable [and monstrously bullish] amount by Ted's discovery of the approximately 1.2 billion troy ounce physical short position in silver that Bank of America appears to hold in the OTC market...along with the big increase in Goldman's derivatives position in silver in that market, as shown in last Friday's OCC Report...which Ted figures is a long position.

He has also come to the conclusion that BofA is short about 30 million ounces of gold in the OTC market as well.

The situation regarding the Big 4/8 shorts in silver, gold [and platinum] continues to be far beyond obscene, twisted and grotesque -- and as Ted correctly points out ad nauseam, its resolution will be the sole determinant of precious metal prices going forward.

As always, nothing else matters.

![]()

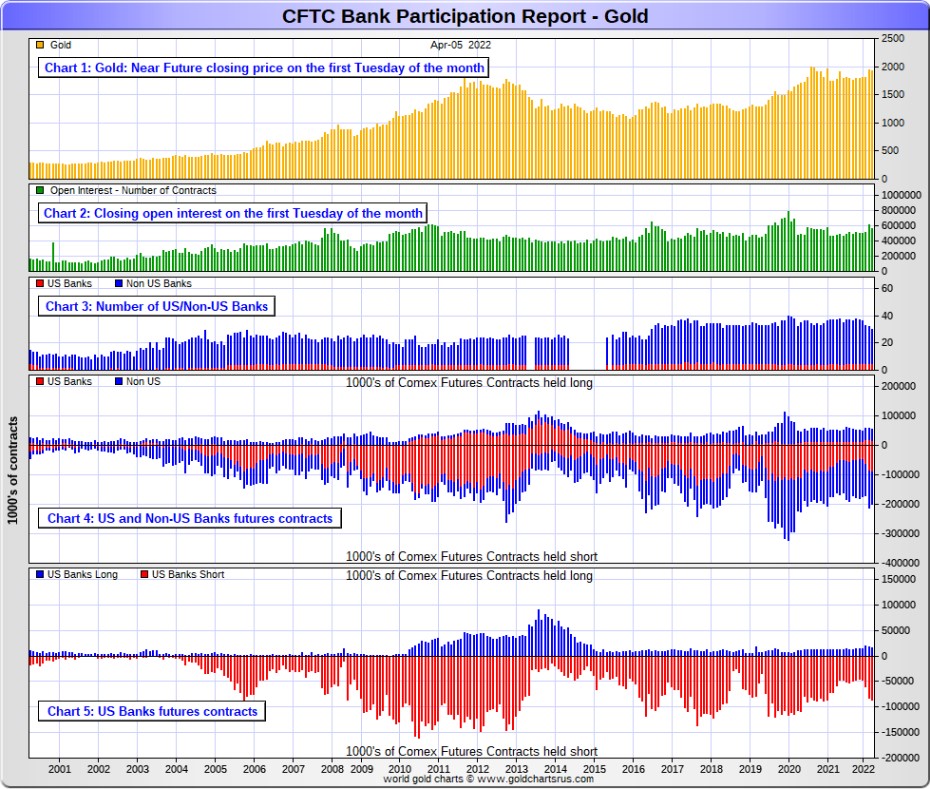

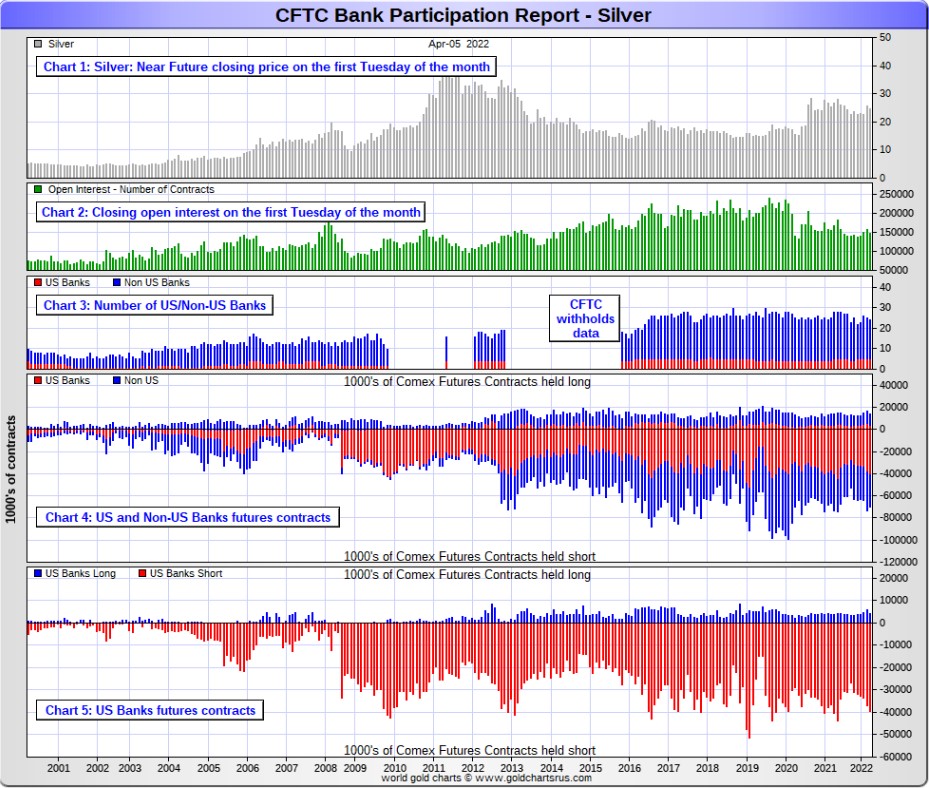

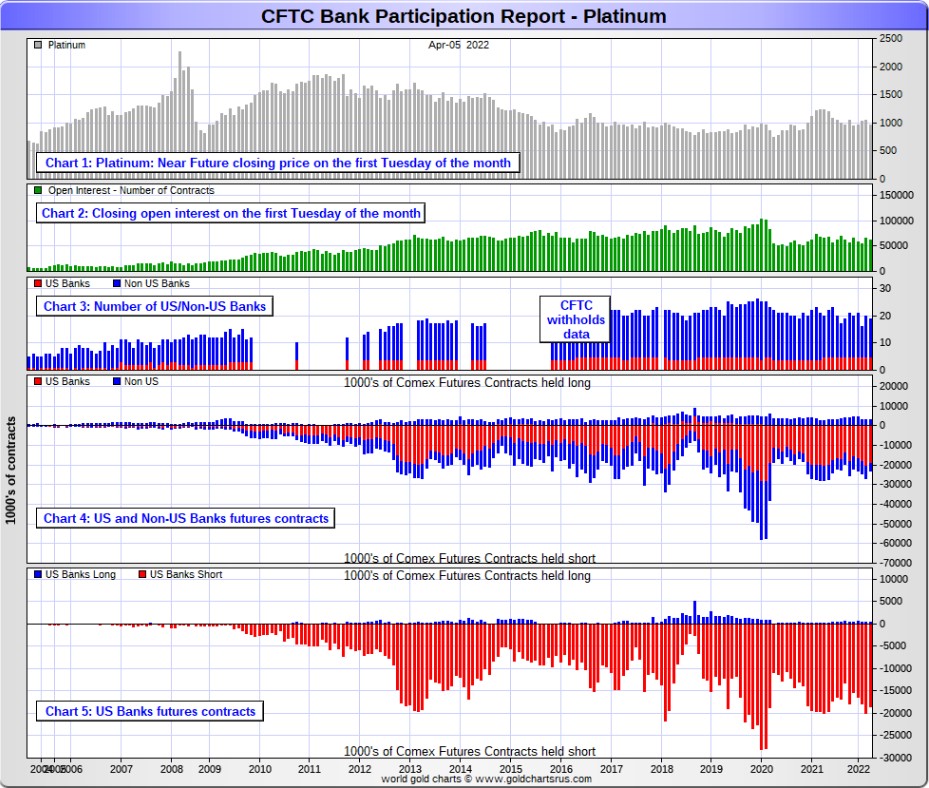

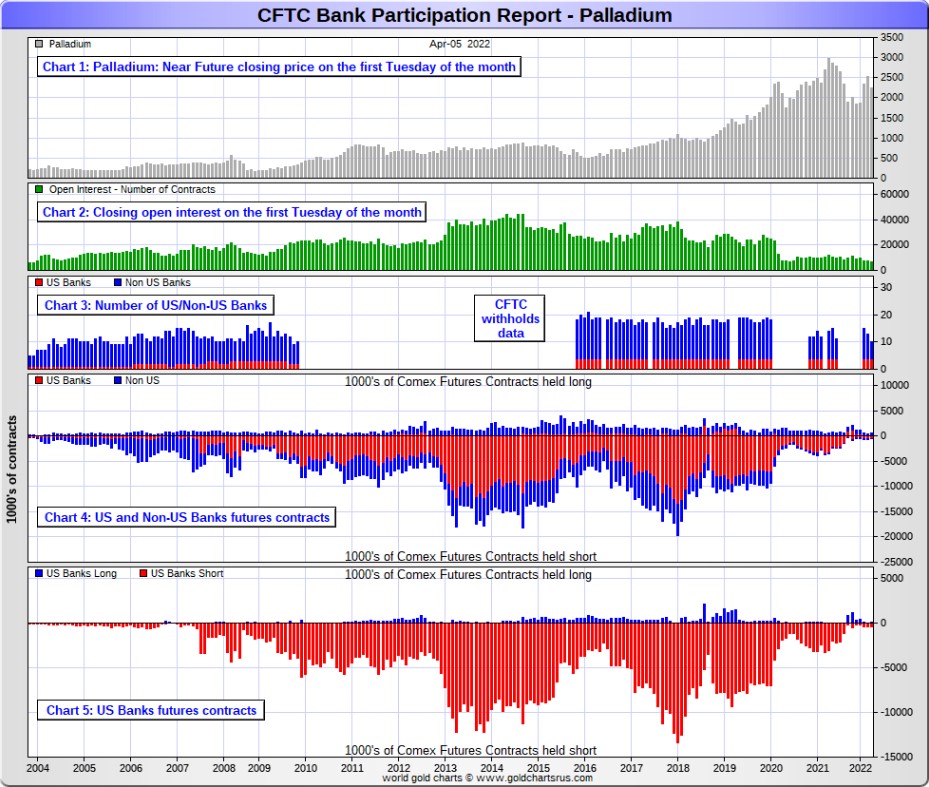

The April Bank Participation Report [BPR] data is extracted directly from yesterday's Commitment of Traders Report. It shows the number of futures contracts, both long and short, that are held by all the U.S. and non-U.S. banks as of Tuesday’s cut-off in all COMEX-traded products. For this one day a month we get to see what the world’s banks are up to in the precious metals. They’re usually up to quite a bit -- and they certainly were this past month.

[The April Bank Participation Report covers the time period from March 1 to April 5 inclusive.]

In gold, 5 U.S. banks are net short 71,460 COMEX contracts in the April BPR. In March’s Bank Participation Report [BPR] these same 5 U.S. banks were net short 64,587 contracts, so there was an increase of 6,873 COMEX contracts month-over-month. That's the fourth month in a row that the U.S. banks have increased their short position in gold.

Citigroup, HSBC USA, Bank of America and Morgan Stanley would most likely be the U.S. banks that are short this amount of gold. I still have my usual suspicions about the Exchange Stabilization Fund, although if they're involved, they are most likely just backstopping these banks.

Also in gold, 25 non-U.S. banks are net short 75,145 COMEX gold contracts. In March's BPR, 27 non-U.S. banks were net short 92,025 contracts...so the month-over-month change shows a big decrease of 16,880 COMEX contracts.

At the low back in the August 2018 BPR...these same non-U.S. banks held a net short position in gold of only 1,960 contacts -- and they've been back on the short side in an enormous way ever since.

I suspect that there's at least three large banks in this group, HSBC, Barclays and Deutsche Bank. I also have my suspicions about Scotiabank/Scotia Capital, Dutch Bank ABN Amro, French bank BNP Paribas, plus Australia's Macquarie Futures. Other than that small handful, the short positions in gold held by the vast majority of non-U.S. banks are immaterial and, like in silver, have always been so.

As of this Bank Participation Report, 30 banks [both U.S. and foreign] are net short 26.2 percent of the entire open interest in gold in the COMEX futures market, which is up a bit from the 25.4 percent that 32 banks were net short in the March BPR.

Here’s Nick’s BPR chart for gold going back to 2000. Charts #4 and #5 are the key ones here. Note the blow-out in the short positions of the non-U.S. banks [the blue bars in chart #4] when Scotiabank’s COMEX short position was outed by the CFTC in October of 2012. Click to enlarge.

In silver, 5 U.S. banks are net short 35,475 COMEX contracts in April's BPR. In March's BPR, the net short position of these same 5 U.S. banks was 31,126 contracts, which is up another 4,349 COMEX contracts month-over-month. This is the third month a row where the short position held by these big 5 U.S. banks has increased...but not by an overly large amount.

The biggest short holders in silver of the five U.S. banks in total, would be Citigroup, HSBC USA, Bank of America, Morgan Stanley...and maybe Goldman Sachs...but not JPMorgan according to Ted. And, like in gold, I have my suspicions about the Exchange Stabilization Fund's role in all this...although, also like in gold, not directly.

Also in silver, 19 non-U.S. banks are net short 21,002 COMEX contracts in the April BPR...which is down a pretty decent amount from the 26,224 contracts that 20 non-U.S. banks were short in the March BPR.

I would suspect that HSBC and Barclays holds a goodly chunk of the short position of these non-U.S. banks...plus some by Canada's Scotiabank/Scotia Capital still. I'm not sure about Deutsche Bank... but now suspect Australia's Macquarie Futures. I'm also of the opinion that a number of the remaining non-U.S. banks may actually be net long the COMEX futures market in silver. But even if they aren’t, the remaining short positions divided up between these other 14 or so non-U.S. banks are immaterial — and have always been so.

As of April's Bank Participation Report, 24 banks [both U.S. and foreign] are net short 38.0 percent of the entire open interest in the COMEX futures market in silver— up a bit from the 36.4 percent that 25 banks were net short in the March BPR. And much, much more than the lion’s share of that is held by Citigroup, HSBC, Bank of America, Barclays -- and Scotiabank -- and possibly one other non-U.S. bank...all of which are card-carrying members of the Big 8 shorts.

I'll point out here that Goldman Sachs, up until late last year, had no derivatives in the COMEX futures market in any of the four precious metals. But they did show up in the last two OCC Reports. Now they have a $4.8 billion position, mostly in silver -- and as I pointed out a bit further up, Ted thinks they're long the market.

Here’s the BPR chart for silver. Note in Chart #4 the blow-out in the non-U.S. bank short position [blue bars] in October of 2012 when Scotiabank was brought in from the cold. Also note August 2008 when JPMorgan took over the silver short position of Bear Stearns—the red bars. It’s very noticeable in Chart #4—and really stands out like the proverbial sore thumb it is in chart #5. But, according to Ted, as of March 2020...they're out of their short positions, not only in silver, but the other three precious metals as well. Click to enlarge.

In platinum, 5 U.S. banks are net short 18,119 COMEX contracts in the April Bank Participation Report, which is down 1,503 contracts from the 19,622 COMEX contracts that these same 5 U.S. banks were short in the March BPR.

I will point out here that this is the first month of the last four that these 5 U.S. banks have decreased their collective short positions in platinum...the Big 8 shorts No. 2 problem child after silver.

At the 'low' back in July of 2018, these U.S. banks were actually net long the platinum market by 2,573 contracts. So they have a very long way to go to get back to just market neutral in platinum...if they ever intend to, that is.

Also in platinum, 14 non-U.S. banks are net short 2,233 COMEX contracts in the April BPR, which is down 1,727 contracts from the 3,960 COMEX contracts that 15 non-U.S. banks were net short in the March BPR.

[Note: Back at the July 2018 low, these same non-U.S. banks were net short only 1,192 COMEX contracts in platinum, so they're closing in on that number again.]

And as of April's Bank Participation Report, 19 banks [both U.S. and foreign] are net short 33.3 percent of platinum's total open interest in the COMEX futures market, which is down a bit from the 36.1 percent that 20 banks were net short in March's BPR.

But it's the U.S. banks that are on the short hook big time -- and the real price managers. They have little chance of delivering into their short positions, although a very large number of platinum contracts have already been delivered during the last year or so...including this current delivery month. But that fact, like in both silver and gold, has made no difference whatsoever to their short positions held. The situation for them in this precious metal is as equally dire in the COMEX futures market as it is with the other two precious metals...silver and gold...particularly the former.

The reason that they'll never improve their short positions in a big way is the same reason as in gold and silver...the Managed Money traders flatly refuse to go short big time like they used to in the past -- and they're actually net long about 5,400 COMEX contracts at the moment.

Here's the Bank Participation Report chart for platinum. Click to enlarge.

In palladium, 4 U.S. banks are net short 318 COMEX contracts, down 67 contracts from the 385 contracts that they were short in March's BPR.

Also in palladium, 6 non-U.S. banks are net long 281 COMEX contracts in the April BPR, up from 9 non-U.S. banks that were net long 130 contracts in March.

Except in February's Bank Participation Report, these non-U.S. banks have been net long palladium by a bit for the last 24 months.

And as I've been commenting for almost forever now, the COMEX futures market in palladium is a market in name only, because it's so illiquid and thinly-traded. Its total open interest at Tuesday's cut-off was only 6,642 contracts...compared to 60,983 contracts of total open interest in platinum...148,526 contracts in silver -- and 560,666 COMEX contracts in gold.

The only reason that there's a futures market at all in palladium, is so that the Big 8 traders can control its price. That's all there is, there ain't no more.

As of this Bank Participation Report, 10 banks [both U.S. and foreign] are net short 0.6 percent of the entire COMEX open interest in palladium...compared to the 1.8 percent of total open interest that 13 banks werenet short in March's BPR.

And because of the small numbers of contracts involved, along with a tiny open interest, these numbers are pretty much meaningless.

But, having said that, for the last two years in a row, the world's banks have not been involved in the palladium market in a material way. It's all hedge funds and commodity trading houses now.

Here’s the palladium BPR chart. Although the world's banks are market neutral at the moment, it remains to be seen if they return as big short sellers again at some point like they've done in the past. Click to enlarge.

Excluding palladium for obvious reasons, only a small handful of the world's banks, most likely four or so in total -- and mostly U.S-based, except for HSBC, Barclays and maybe Deutsche Bank...continue to have meaningful short positions in the other three precious metals. It's a near certainty that they run this price management scheme from within their own in-house/proprietary trading desks...although it's a given that some of their their clients are short these metals as well.

The futures positions in silver and gold that JPMorgan holds are immaterial -- and have been since March of 2020...according to Ted Butler. And what net positions they might hold, would certainly be on the long side of the market. It's the new 7+1 shorts et al. that are on the hook in everything precious metals-related.

And as has been the case for years now, the short positions held by the Big 4/8 traders/banks is the only thing that matters...especially the short positions of the Big 4 -- and how it is ultimately resolved [as Ted said earlier] will be the sole determinant of precious metal prices going forward.

The Big 8 shorts, along with Ted's raptors...the small commercial traders other than the Big 8 commercial shorts...continue to have an iron grip on their respective prices -- and nothing has changed in that regard over the last month...at least what can be seen on the surface. They continue to be the cork in the precious metal price bottle.

That situation will persist until they either voluntarily give it up...or are told to step aside, as it now appears that there's no chance that they will ever get overrun. If that possibility had ever existed in reality, it would have happened already. However, considering the current state of affairs in the world today -- and the physical shortage in silver, I suppose one shouldn't rule it out entirely.

I have a very large number of stories, articles and videos for you today, including quite a few I've been saving for today's column for length and/or content reason.

![]()

CRITICAL READS...

Read the full article on SilverSeek.com: "Battle Stations" For 'Da Boyz' in New York on Friday

About the author