The days of paying for something with cold, hard cash may be numbered. The pandemic has accelerated our transition towards a cashless economy, with consumers nowadays preferring the convenience of mobile banking or digital wallets.

Today, roughly 41% of Americans say none of their purchases in a typical week are paid for using cash, up from 29% in 2018 and 24% in 2015, according to a new Pew Research Center survey.

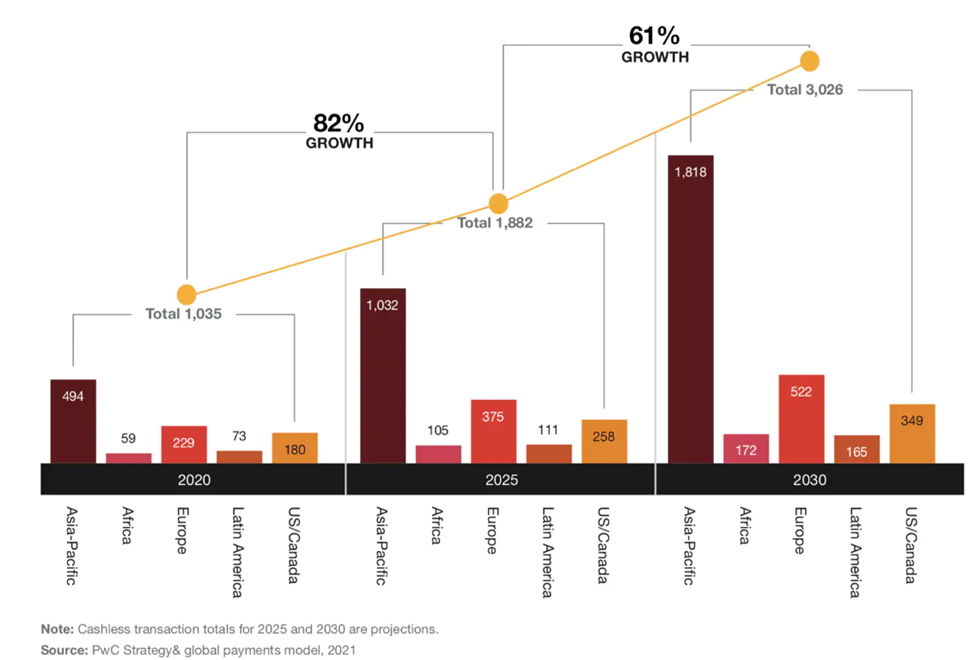

Here in Canada, cash purchases are expected to make up only 10% of money spent by 2030, according to Moneris, the nation’s leading credit and debit card processor. Globally, cashless payment volumes are set to increase by more than 80% from 2020 to 2025, and to almost triple by 2030, a study by PwC found.

Source: PwC

Source: PwC

And as digital payment technologies continue to advance, it’s only a matter of time before cash payments are completely discarded. But for a cashless economy to really thrive, there would need to be support from the central banks that govern the money supply of their respective nations.

Taking notes from the emergence of cryptocurrency and blockchain technology, many countries have already started looking at ways to integrate themselves into this new economy, beginning with their own digital currency.

Central Bank Digital Currencies

The idea behind central bank digital currencies (CBDCs) is to implement a payment system that has both the transactional convenience of digital currencies and the financial security of fiat currencies. CBDCs would essentially serve as a digital form of a government-issued currency that isn’t pegged to any physical commodity.

According to Investopedia, CBDCs can take two forms: wholesale and retail. Wholesale CBDCs are similar to holding reserves in a central bank. The central bank grants an institution an account to deposit funds or use to settle interbank transfers. Central banks can then use monetary policy tools to influence lending and set interest rates. These are primarily used by financial institutions.

Retail CBDCs are government-backed digital currencies used by consumers and businesses. They eliminate intermediary risk — the risk that private digital currency issuers might become bankrupt and lose customers’ assets. These are used by consumers and businesses, much like fiat currency.

There are two approaches being taken by countries when it comes to retail CBDCs. Token-based CBDCs (such as DCash used in the Eastern Caribbean) are accessible with private/public keys as a method of validation for users to execute transactions anonymously, while account-based CBDCs (like China’s e-CNY) require digital identification to access an account.

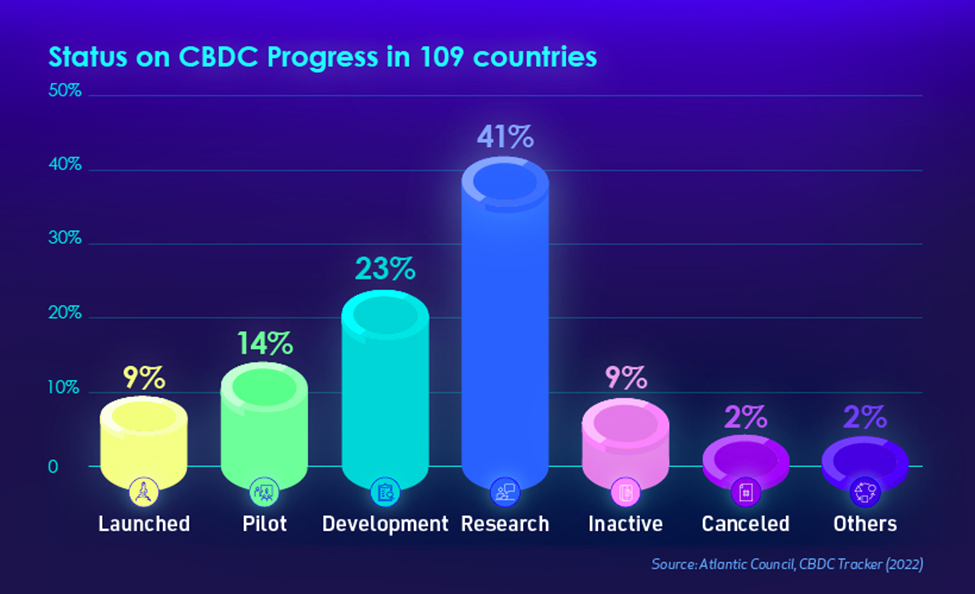

As many as 114 countries—representing more than 95% of global GDP—are exploring CBDCs right now, according to the Atlantic Council, a US-based think tank.

So far, eleven countries have fully launched a digital currency, with Jamaica being the latest to do so and the first to be ratified formally as legal tender. China, which has already started large-scale trials of its “e-yuan”, is expected to expand to most of the country in 2023.

Credit: Statista

Credit: Statista

As of December 2022, all G7 economies have moved into the development stage of a CBDC. The New York Federal Reserve’s wholesale CBDC experiment, Project Cedar, has shifted from research into development.

According to the Atlantic Council, over 20 countries will take significant steps toward piloting a CBDC in 2023. Australia, Thailand, Brazil, India, South Korea and Russia intend to continue or begin pilot testing in 2023.

The European Central Bank is also likely to start a pilot next year for a unique model, in which licensed financial institutions each operate a permissioned node of the blockchain network as a conduit for the distribution of a digital euro.

Source: Visual Capitalist

Source: Visual Capitalist

Benefits of Going Digital

According to McKinsey, there are four trends that likely spurred central banks’ interest in adopting CBDCs.

First, and the most obvious, is the decline in cash usage across the world. In some places, the change has been much more dramatic. For instance, in Europe, cash usage has plummeted by one-third between 2014 and 2021, while demand for cash in Sweden has dropped by more than 50% over the past decade.

The second driving force is the growing interest in privately issued digital assets. In the United Kingdom, around 10% of adults report holding or having held a digital asset, like cryptocurrency. The ECB says that as many as 10% of households in six large EU countries now own digital assets.

The third is a decreasing sense of central banks as payment innovators. The adoption of CBDCs would offer central banks a new opportunity to lead strategic conversations on cash use cases in a public forum.

The fourth trend is simply the rise in global payment systems. Many central banks are now seeking to establish greater local governance over increasingly global payment systems, and they see CBDC as a potential stabilizing anchor of local digital payment systems.

McKinsey believes that the widespread adoption of CBDCs would lead to a myriad of benefits by addressing many issues related to efficiency, security, and access. Arguably the biggest benefit is reduced costs. Financial-service providers stand to save $400 billion annually in direct costs by shifting spending away from physical infrastructure and toward digital finance, according to the firm’s estimates.

CBDCs would also provide greater access for those without banking accounts. It is estimated that over a billion people around the world are unbanked; under 5% of US adults still don’t have bank accounts. McKinsey says the CBDCs accessible through mobile devices could potentially increase financial inclusion.

Also part of the package is heightened security. Deploying a regulated digital currency accessible via mobile devices could potentially enhance payment security by ensuring that a transaction is finalized and unalterable—even without a formal bank account—reducing the chances of fraud, McKinsey adds.

Rise of International CBDCs?

The fascinating thing about CBDCs is that it’s not exclusively restricted to central banks; any financial agency is capable of undertaking such a project. What’s to stop, say, the International Monetary Fund, which provides policy advice to central banks, from running its own CBDC to rule other national currencies?

While that hasn’t happened yet, the signs are there that the IMF wants in on some of the action. Last week, at the IMF Spring Meetings 2023, the Digital Currency Monetary Authority (DCMA) announced the official launch of an international CBDC that “strengthens the monetary sovereignty of participating central banks and complies with the recent crypto assets policy recommendations proposed by the IMF.”

The Universal Monetary Unit (UMU), symbolized as ANSI Character, Ü, is “legally a money commodity, can transact in any legal tender settlement currency, and functions like a CBDC to enforce banking regulations and to protect the financial integrity of the international banking system,” the DCMA’s official statement said.

The DCMA, which hails itself as the world leader in the advocacy of digital currency and monetary policy innovations for governments and central banks, introduced UMU as Crypto 2.0 because “it innovates a new wave of cryptographic technologies for realizing a digital currency public monetary system with a widespread adoption framework encompassing use cases for all constituencies in a global economy.”

While the UMU is not created by the IMF, the fact that it was unveiled at one of its gatherings has raised alarm bells as to the authenticity of CBDCs and the potential lack of barriers to entry.

Few details have also been given regarding the constituents of the DCMA, except that its membership consists of sovereign states, central banks, commercial and retail banks, and other financial institutions.

Many are of the opinion that such a move, in conjunction with Western governments all exploring CBDCs at the same time, can’t just be a coincidence. Could this all be part of a grander plan to establish the IMF’s hold on the global financial system? Especially seeing that China’s digital currency is much farther ahead in development?

Implications on Gold

Western political correspondents are of the view that a full launch of the “e-yuan” could serve as another weapon used by China against its Western rivals.

Like all CBDCs, the Chinese digital currency strips users of their financial privacy; all payment activity involving e-CNY can be seen by the People’s Bank of China, and will be stored in its database.

The concern is not necessarily the few American citizens that make payments in e-CNY, but the US firms that operate in China, which are already being pressured to use or accept e-CNY. Hence, they are very much subject to surveillance in that sense.

“The digital yuan is the largest threat to the West that we’ve faced in the last 30, 40 years. It allows China to get their claws into everyone in the West and allows them to export their digital authoritarianism,” an analyst at Hayman Capital Management told CNBC back in 2021.

Another reason for concern is the threat that China’s currency has on the US dollar and its role as the monetary leader in the global economy. At Ahead of the Herd, we believe that a global de-dollarization is already upon us with the growing reluctance by non-Western nations to use the greenback.

Many central banks have already sought alternatives to the primary reserve currency, and gold is the ideal choice given its history with USD.

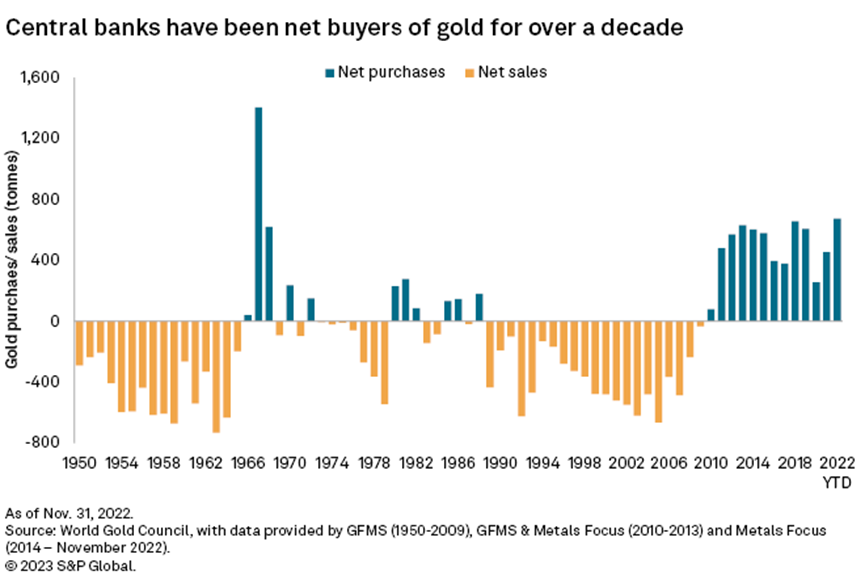

Last year, global central banks bought the most gold on record, at a whopping 1,136 tonnes valued at some $70 billion, according to the World Gold Council. The stockpiling of gold continued at a record pace in 2023, with the banks adding another 125 tonnes during the first two months.

Source: S&P Global

Source: S&P Global

Interestingly, data available to the WGC revealed that there is indeed a West-to-East migration of gold in the recent buying pattern, highlighted by China’s rare reporting of gold purchases, which has now extended to four straight months.

According to the latest WGC data, the largest purchases in the first two months of 2023 were made by non-Western nations: Singapore (51.4 tonnes), Turkey (45.5 tonnes), China (39.8 tonnes), Russia (31.1 tonnes) and India (2.8 tonnes).

Many analysts believe that a large portion of China’s purchases remains unreported, and the country is the “mystery buyer” stockpiling gold in recent years to minimize its exposure to the US dollar.

Investors, too, could lean towards gold simply because of their disdain, and more importantly, distrust, for government-issued digital currencies. As we discussed before, CBDCs, just like fiat money, are supported by trust, and it would make no sense for them to not be backed by any hard assets.

China appears to be the first nation to realize this and is rushing to accumulate as much gold as it can. The country is “officially” the fifth largest gold holder, but since it rarely makes public its purchases, who knows how much gold Beijing really holds?

While we can only speculate at this juncture, it would make sense for China to eventually use its gold reserves to back its digital currency e-CNY, whose progress has gained much attention since trials started in 2019.

All in all, it seems as though the global push for central bank digital currencies could offer further support for gold prices, which are approaching record highs.

Central banks will continue buying the precious metal as part of their diversification strategy, while investors will like its hedging appeal in an environment where the fate of both fiat and digital currencies poses risks.

Richard (Rick) Mills

aheadoftheherd.com

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

AOTH/Richard Mills has based this document on information obtained from sources he believes to be reliable, but which has not been independently verified.

AOTH/Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness.

Expressions of opinion are those of AOTH/Richard Mills only and are subject to change without notice.

AOTH/Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, AOTH/Richard Mills assumes no liability for any direct or indirect loss or damage for lost profit, which you may incur as a result of the use and existence of the information provided within this AOTH/Richard Mills Report.

You agree that by reading AOTH/Richard Mills articles, you are acting at your OWN RISK. In no event should AOTH/Richard Mills liable for any direct or indirect trading losses caused by any information contained in AOTH/Richard Mills articles. Information in AOTH/Richard Mills articles is not an offer to sell or a solicitation of an offer to buy any security. AOTH/Richard Mills is not suggesting the transacting of any financial instruments.

Our publications are not a recommendation to buy or sell a security – no information posted on this site is to be considered investment advice or a recommendation to do anything involving finance or money aside from performing your own due diligence and consulting with your personal registered broker/financial advisor.

AOTH/Richard Mills recommends that before investing in any securities, you consult with a professional financial planner or advisor, and that you should conduct a complete and independent investigation before investing in any security after prudent consideration of all pertinent risks. Ahead of the Herd is not a registered broker, dealer, analyst, or advisor. We hold no investment licenses and may not sell, offer to sell, or offer to buy any security.

About the author

Richard (Rick) Mills

Legal Notice / Disclaimer

Ahead of the Herd newsletter, aheadoftheherd.com, hereafter known as AOTH.

Please read the entire Disclaimer carefully before you use this website or read the newsletter. If you do not agree to all the AOTH/Richard Mills Disclaimer, do not access/read this website/newsletter/article, or any of its pages. By reading/using this AOTH/Richard Mills website/newsletter/article, and whether or not you actually read this Disclaimer, you are deemed to have accepted it.

Any AOTH/Richard Mills document is not, and should not be, construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.